What Is The Uk Average Credit Score

Ever thought about your credit score like a secret superpower? It’s not quite a cape and a mask, but in the grown-up world of finance, it’s surprisingly important. Imagine it as your financial report card, a quick snapshot of how you’ve handled money in the past. Lenders, like banks or companies offering you a phone contract, peek at this report card to see if you’re a good bet.

So, what’s the magic number everyone’s chasing? The truth is, there isn't one single UK average credit score that’s universally agreed upon. It's a bit like asking for the average height of a British person – it depends on who you ask and which survey you look at! But, to give you a general idea, most experts point towards a range that suggests you're doing pretty well.

Think of it like this: your credit score is a number between 0 and 1,000 (or sometimes 700, depending on the scoring system). The higher the number, the happier the lenders are. A really low score might make them a little nervous, like a cat spotting a cucumber.

Must Read

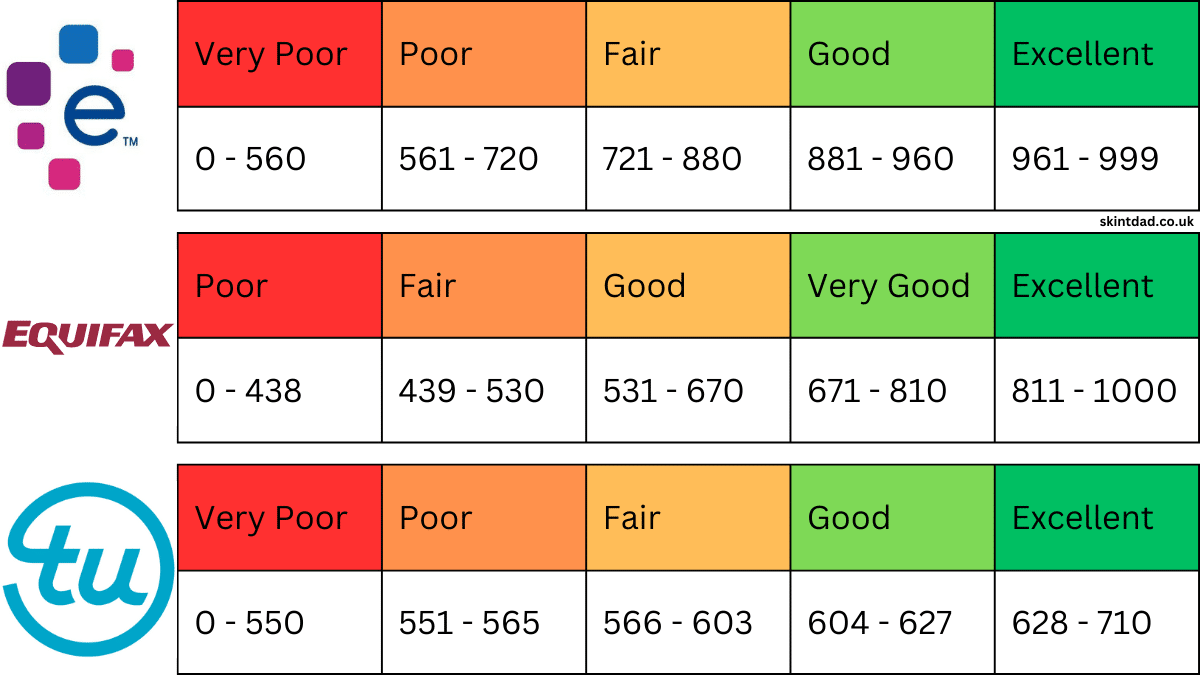

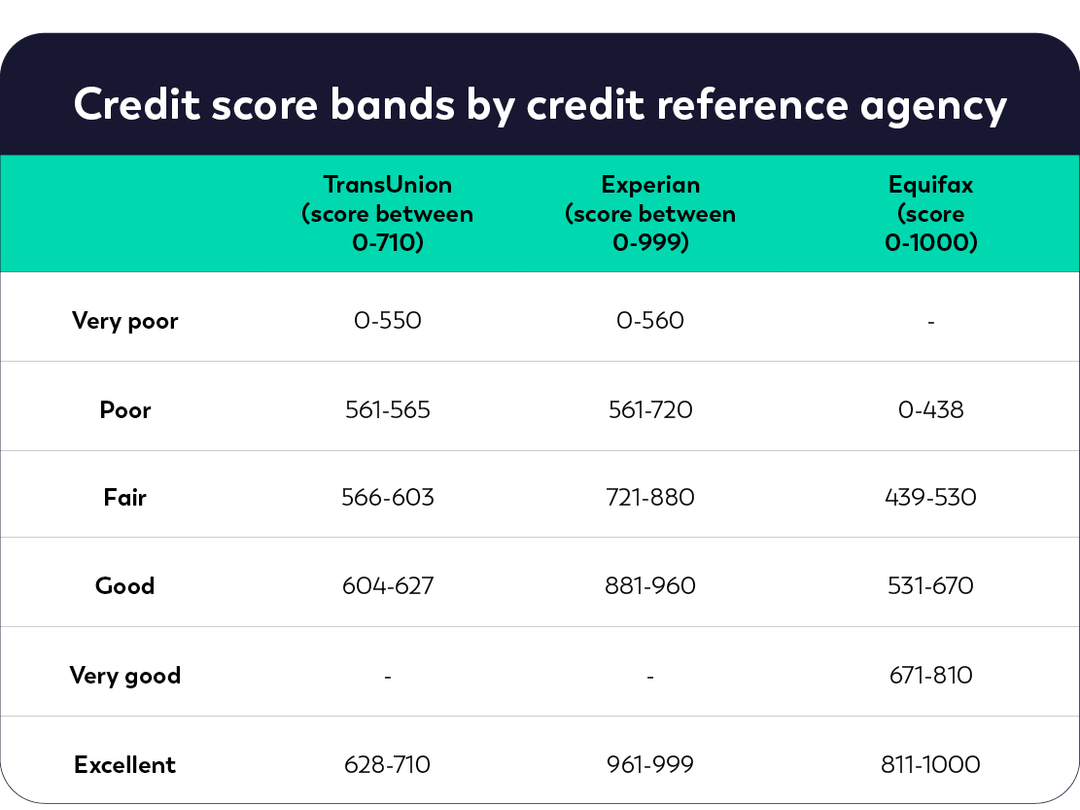

We’re talking about the big three credit reference agencies in the UK: Experian, Equifax, and TransUnion. Each of them has its own way of calculating your score, using slightly different algorithms and data. It’s like three different teachers marking the same essay, and they might give you slightly different grades.

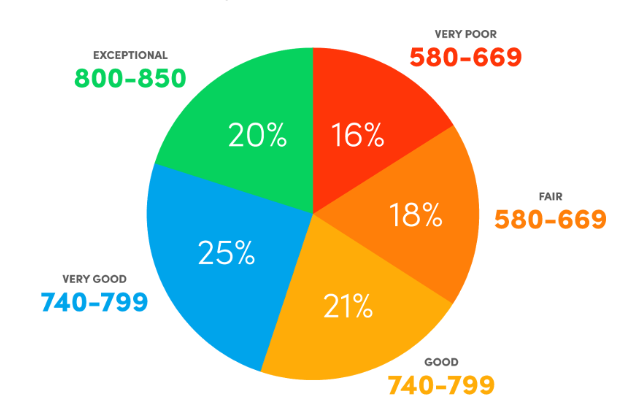

However, for a ballpark figure, if you’re looking at a score between 881 and 960, you’re generally in the ‘excellent’ category with most of these agencies. This is the sweet spot, the VIP lounge of credit scores. It means you’re practically a financial superstar, a real money-wizard!

What does this ‘excellent’ score actually mean for you? It means you’re likely to be offered the best deals. Think lower interest rates on loans, better credit card offers with more perks, and even easier approval for mortgages or rental agreements. It’s like having a golden ticket, opening doors to all sorts of financial goodies.

On the flip side, what’s considered a ‘poor’ score? Generally, anything below 561 might be considered a red flag. This doesn’t mean you’re a terrible person, just that lenders see a higher risk. It might make getting credit a bit trickier, and the terms you are offered could be less favourable.

Now, let’s sprinkle in some heartwarming and humorous bits. Did you know that getting your first credit card and using it responsibly is like your first step towards financial independence? It’s a rite of passage, much like learning to ride a bike. Initially wobbly, but with practice, you glide along smoothly.

And the surprising part? Your credit score isn’t just about big loans or mortgages. It can also impact things like your mobile phone contract or even your insurance premiums. So, that seemingly small decision to pay your bill on time every month is actually building your financial reputation, brick by brick.

Imagine a lender looking at your score. If it’s sky-high, they might be practically throwing offers at you. "Here, have this amazing credit card with 0% interest for a year!" they might exclaim, with a twinkle in their eye. If it's lower, they might be a bit more cautious, like a squirrel hoarding nuts for winter, wanting to make sure they get their acorns back.

The heartwarming aspect is that your credit score is something you can actively improve. It’s not set in stone. Every responsible financial decision you make is like planting a seed that will grow into a money-tree. It takes time and patience, but the rewards are substantial.

So, how do you get into that ‘excellent’ bracket, or at least move towards it? It’s not rocket science. The golden rules are simple and surprisingly effective:

First and foremost, pay all your bills on time, every time. This includes credit cards, utility bills, and any other regular payments. Late payments are like tripping over your own feet – they’ll definitely bring your score down.

Secondly, keep your credit utilisation low. This means don’t max out your credit cards. Ideally, aim to use less than 30% of your available credit limit. Think of it as a credit diet – don’t overindulge!

Thirdly, don’t apply for too much credit all at once. Every time you apply for credit, it leaves a little mark on your report. Spreading out applications is like spreading out your requests for treats – it looks less desperate.

Fourthly, check your credit reports regularly. You can get free copies from the main agencies. It’s like doing a regular check-up on your financial health to spot any potential issues early. You might even find a surprise or two!

And finally, be mindful of your electoral roll registration. Being on the electoral roll helps agencies confirm your identity and address, which is a positive sign for lenders.

It’s fascinating to think about how these numbers are built. They reflect a history of your financial behaviour, a narrative written in digits. Every loan you’ve repaid, every bill settled, contributes to this ongoing story.

Imagine your credit score as a proud parent looking at their child’s achievements. When you manage your money well, your credit score is doing a happy little dance, and the lenders are nodding in approval.

The concept of a "UK average" credit score is a bit elusive, as we've discussed. However, general consensus suggests that a score in the high 800s to mid-900s with Experian, for instance, is considered excellent. Equifax and TransUnion have slightly different scales, but the principle remains the same: higher is better.

It’s not about perfection, though. Life happens. Sometimes, unexpected expenses pop up, and a payment might be a few days late. The key is consistency and demonstrating that you can recover and continue to be responsible.

Think of it like a well-loved teddy bear. It might have a few stitches here and there, a bit of wear and tear from years of hugs, but its overall condition is still very good. That’s how lenders often view a good credit score with a minor imperfection – still a trustworthy companion.

So, while the exact UK average might be a moving target, the aspiration is clear: a strong credit score. It's your financial reputation, your silent endorsement, and a powerful tool in your financial arsenal. It’s less about a specific number and more about building a trustworthy financial history.

Embrace the journey of building and maintaining a good credit score. It’s a small effort with a big payoff, allowing you to access better financial products and live a life with fewer financial hurdles. And who knows, you might even find a little joy in watching those numbers climb!

Ultimately, your credit score is a reflection of your financial diligence. It’s a story of responsibility and trustworthiness, a tale that lenders are always eager to read. And with a little effort and smart choices, your story can be one of financial success.

![What's the Average Credit Score UK Citizens Have? [21 Stats]](https://review42.com/wp-content/uploads/2021/11/feature-image-2-uk-credit-score-statistics.jpg)