What Is Compulsory Excess On Car Insurance

Ever found yourself staring at your car insurance documents, a little bewildered by all the jargon? Yeah, me too. It’s like trying to decipher an ancient scroll, isn't it? One of those terms that pops up and makes you squint is "compulsory excess." Sounds a bit… well, compulsory, and maybe a bit excessive, right? Let’s break it down in a way that’s as easy-going as a Sunday drive.

Imagine you’ve just bought a brand new, shiny car. You’re practically floating on air. Then, oops! You’re backing out of your driveway and bonk – you’ve nudged the garden gnome collection. Your heart sinks. You’ll need to get that bumper sorted, and that means calling your insurance company.

Now, when you make a claim, there’s usually a bit of the bill that you have to chip in. That's where the excess comes in. Think of it like your friendly contribution to fixing the mishap. It’s the first chunk of money you pay towards a repair or a replacement before your insurance company steps in to cover the rest.

Must Read

So, What Exactly is "Compulsory Excess"?

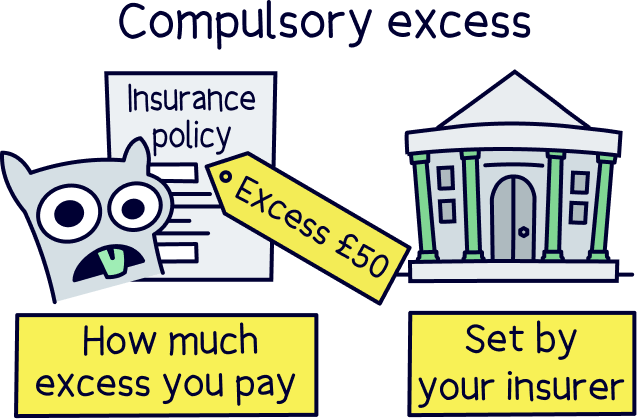

The "compulsory" part is the key here. This isn't an optional extra, like adding heated seats to your car. This is a non-negotiable amount that your insurer expects you to pay. It’s often set by the insurance company itself and is a standard part of your policy. You can’t really haggle over it – it’s just there.

Think of it like a subscription service. Some services offer a free trial, and then you pay a monthly fee. Or, maybe you’ve got a mobile phone contract, and if you lose it, you might have to pay a certain amount towards a replacement, regardless of how new it was. The compulsory excess works in a similar fashion for your car insurance. It’s the basic amount you’re on the hook for.

Why Does It Exist?

Why do insurers make us pay this? Well, it’s a few things, really. Firstly, it helps them keep your premiums lower. If everyone paid the full whack for every tiny scratch, insurance costs would skyrocket for all of us. By sharing a little bit of the cost, insurers can offer more affordable policies. It’s a bit like a neighborhood watch – if everyone looks out for their own little bit, the whole street is safer and more peaceful (and probably cheaper to maintain!).

Secondly, it discourages small, frivolous claims. Imagine if every time a bird did its business on your windscreen, you filed a claim. It would be chaos! The excess acts as a small hurdle, making people think twice before claiming for minor incidents. It encourages us to use our common sense and perhaps use a sponge and some soapy water instead of a full-blown insurance claim for a pesky pigeon dropping.

Think of it like this: you know that feeling when you're about to send a slightly cheeky email, but you pause and think, "Hmm, maybe not"? The compulsory excess is the insurance world's version of that polite pause. It’s a gentle nudge to say, "Is this claim really worth it?"

What Happens When You Make a Claim?

Let's say your compulsory excess is £250. If you have a fender bender and the repair bill comes to £1,000, here’s how it plays out:

- You'll pay the first £250 (your compulsory excess).

- Your insurance company will then cover the remaining £750.

So, in this scenario, your out-of-pocket cost is £250. Simple, right?

But what if the damage is less than your excess? If a rogue shopping trolley leaves a tiny scratch that costs £150 to fix, and your excess is £250, you’ll be paying the full £150 yourself. Your insurance company won't pay out in this instance because the repair cost is lower than your agreed-upon excess. It's like trying to use a coupon for 50% off a single sweet – it’s just not worth the paperwork for the shop!

Is There Anything Else I Should Know?

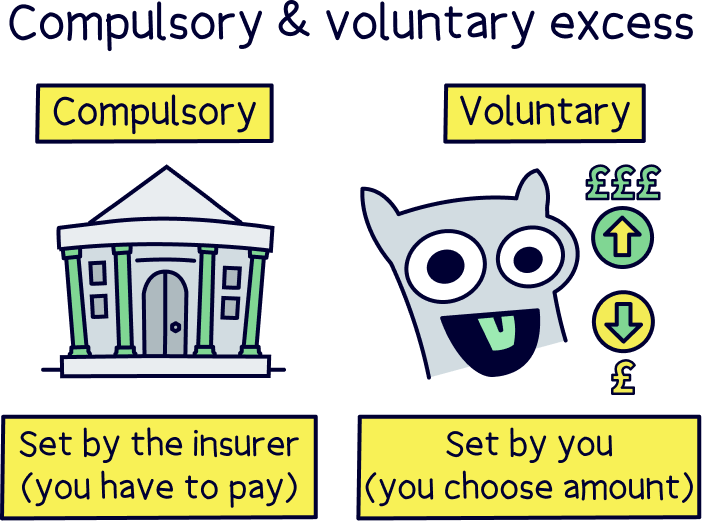

Yes! Sometimes, you might see another type of excess called an "voluntary excess." This is the extra amount you can choose to pay on top of your compulsory excess. Why would you do that? Well, offering to pay a higher voluntary excess usually means your premiums will be lower. It’s a trade-off: you pay a bit more upfront if something happens, but you save a bit more regularly.

Think of it like deciding how much "tip" you want to leave at a restaurant. The compulsory excess is like the automatic service charge that’s always there. The voluntary excess is like deciding to add a little extra yourself to show you’re willing to contribute more, and in return, maybe you get a slightly better deal on the main bill (your insurance premium).

It's always a good idea to understand both your compulsory and any voluntary excess you've agreed to. This way, you won’t be caught off guard if you ever need to make a claim. It’s like packing an umbrella even when it’s sunny – you might not need it, but it’s good to have it just in case!

Why Should You Care?

You should care about compulsory excess because it directly impacts your finances. Knowing this amount is crucial for budgeting and making informed decisions about your insurance. If you have a higher compulsory excess, you'll likely have lower annual premiums. However, if you make a claim, you'll have to pay a larger chunk of the repair cost upfront.

It’s a balancing act. For some people, especially those who are careful drivers and haven't made claims for years, opting for a higher excess (by increasing their voluntary excess) can lead to significant savings. For others, who might be newer drivers or want the peace of mind of a lower out-of-pocket cost in case of an accident, a lower excess might be preferable, even if it means slightly higher premiums.

Imagine you're planning a big party. You know you'll need to buy decorations, food, and drinks. That's like your insurance premiums. Now, imagine you know you might have some unexpected guests arrive. That’s like an accident. The compulsory excess is the amount you’ve decided you’re prepared to spend on those unexpected guests. Knowing that amount helps you plan your overall party budget better.

So, next time you’re looking at your car insurance, don’t just skim over that "compulsory excess" figure. Take a moment to understand what it means for you. It’s not a scary monster; it’s just a smart financial tool that helps keep your insurance affordable and ensures you and your insurer are on the same page when it comes to sharing the cost of any bumps in the road. And that, my friends, is worth knowing!

.jpg)