Regions Bank 30 Year Mortgage Rates

Hey there, homebuyer extraordinaire! So, you’re thinking about diving into the world of mortgages, and the big 3-0 keeps popping up, right? Thirty-year mortgages – they’re like that reliable old friend who’s always there. And when you’re looking at Regions Bank for your mortgage journey, you’re probably wondering, “What’s the deal with their 30-year rates?” Well, pull up a comfy chair (maybe one you’re already paying off with rent, but soon to be your own!), grab a cuppa, and let’s chat about it. No jargon-filled lectures here, just good old-fashioned real talk.

Think of a 30-year mortgage as the marathon runner of home loans. It’s going to take you a while to cross the finish line, but it breaks down those massive payments into smaller, more manageable chunks. This is usually the go-to for a lot of folks because, let's be honest, buying a house is a big deal, and spreading that cost out over three decades makes it feel a whole lot less like scaling Mount Everest in your flip-flops. Regions Bank, like most lenders, offers this popular option, and it’s a solid choice for many.

Now, let's get to the juicy bit: Regions Bank 30-year mortgage rates. What makes them tick? It’s not like they’re set by a magic eight ball, though sometimes it feels like it, doesn’t it? These rates are influenced by a whole bunch of factors, kind of like a recipe with lots of ingredients. The main chef in charge? The Federal Reserve. Their decisions on interest rates play a massive role. When the Fed hikes rates, mortgage rates tend to follow suit. Think of it as the general market’s mood. A happy, stable market usually means better rates. A nervous, shaky market? Well, you get the idea.

Must Read

Then there’s the whole world of the economy. Unemployment rates, inflation, how many people are buying houses versus how many are selling – all these economic indicators are like the background music to the mortgage rate show. A booming economy with low unemployment might mean slightly higher demand for homes, which can nudge rates up. Conversely, a slower economy might see lenders trying to attract borrowers with more appealing rates.

And don't forget about your own financial situation! This is where you become the star of your own mortgage show. Your credit score is a HUGE deal. The better your credit score, the less risky you appear to the bank, and the better your rate is likely to be. Think of it as your financial report card. A stellar report card (high credit score) gets you a scholarship (lower interest rate). A slightly less stellar one might still get you in, but perhaps with a bit less financial aid.

Regions Bank, bless their hearts, wants to lend you money, but they also want to make sure they get it back. So, they're looking at your debt-to-income ratio (DTI). This is basically how much of your monthly income goes towards paying off debts. If you’ve got a lot of car payments, student loans, and credit card bills already piling up, your DTI might be higher, which could affect your rate. They want to see that you’ve got enough wiggle room in your budget to handle a mortgage payment and still afford your favorite artisanal cheese.

Another biggie is the loan-to-value ratio (LTV). This is the relationship between how much you’re borrowing and the appraised value of the home. A bigger down payment means a lower LTV, and that’s generally good news for your rate. Putting down a hefty chunk of cash says, “Hey, I’m really invested in this!” and lenders like that. They’re less worried about you walking away if they have less of their own money on the line.

So, when you’re looking at Regions Bank 30-year mortgage rates, it’s a dynamic thing. It’s not a static number you see on a billboard. It’s a moving target that’s influenced by global economies, national trends, and, most importantly, you. Think of it like trying to catch a really cool, but slightly elusive, butterfly. You need the right conditions, the right timing, and a little bit of luck!

Now, what kind of rates can you actually expect from Regions? This is where I have to put on my responsible narrator hat for a second (it’s a very stylish hat, by the way). I can’t give you exact numbers because, well, they change faster than a toddler’s mood. What’s true today might be different tomorrow. Plus, as we’ve just discussed, your personal situation is the magic wand that waves over those numbers.

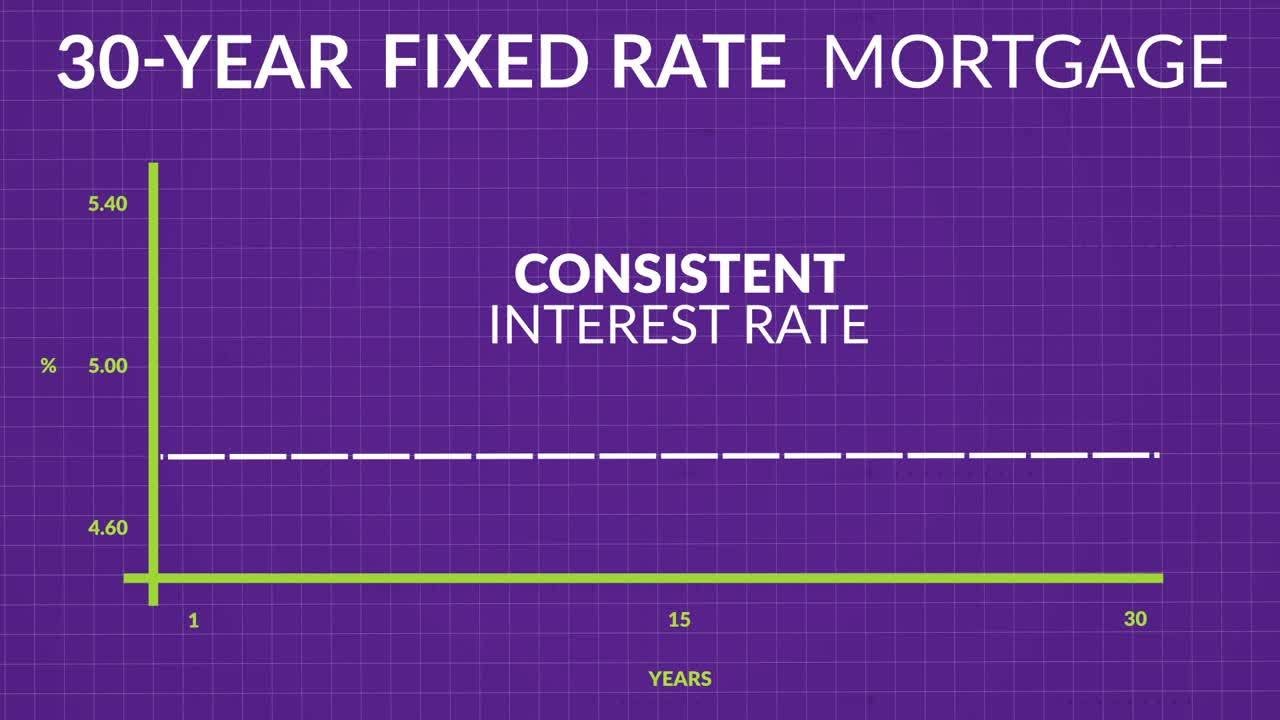

However, I can tell you this: Regions Bank is a major player, and they’re generally competitive. They’re not going to be offering rates that make other banks look like they’re selling gold bars. They want your business! You’ll find that their 30-year fixed-rate mortgages are a cornerstone of their lending offerings. The "fixed" part is super important – it means your interest rate stays the same for the entire 30 years. No surprises! Your principal and interest payment will be the same every single month. It’s like a predictable sitcom episode – you know what you’re getting!

What might you see? You might see rates in the ballpark of what other large national lenders are offering. Sometimes, they might have special promotions or programs. It’s always worth checking their website, or better yet, having a good old-fashioned chat with a mortgage loan officer at Regions. They are the gatekeepers of the current rates and can give you the most up-to-date information. Don’t be shy! Ask them all your burning questions. They’ve heard it all before, probably while juggling a coffee and a bagel. They’re there to help you navigate this maze.

Let’s talk about the 30-year fixed-rate mortgage specifically. Why is it so popular? Well, predictability is a beautiful thing, especially when you’re talking about one of the biggest financial commitments of your life. Your monthly payment for principal and interest will never change. Ever. This makes budgeting a breeze. You can plan your finances years in advance without worrying about your mortgage payment suddenly jumping up like a startled cat. This stability is gold, especially if you’re someone who likes to have a clear financial roadmap.

Of course, there’s a trade-off. Because you’re stretching out those payments over 30 years, you’ll likely end up paying more interest over the life of the loan compared to a shorter-term mortgage, like a 15-year. It’s kind of like buying something on a layaway plan versus paying for it all upfront. You get the item now, but the total cost might be a tad higher because of the extended payment period. However, for many, the lower monthly payment makes homeownership accessible in the first place. It’s a balancing act, right?

When you’re comparing Regions Bank 30-year mortgage rates to others, don't just look at the headline number. Pay attention to the Annual Percentage Rate (APR). The APR is a more comprehensive figure because it includes not just the interest rate but also other fees associated with the loan, like origination fees, points, and private mortgage insurance (PMI) if applicable. Think of the APR as the "total cost of borrowing" number. It gives you a clearer picture of what you'll actually be paying.

Getting pre-approved is another super smart move. This is where Regions Bank will take a look at your financial picture and give you an estimate of how much you can borrow and at what rate. It’s like getting a quote before you order a custom-made suit. It gives you a solid idea of what to expect and helps you narrow down your home search. Plus, sellers love to see pre-approval letters. It shows you’re serious and ready to roll!

Don’t forget about potential closing costs. These are the fees you pay at the very end of the mortgage process to finalize everything. They can include things like appraisal fees, title insurance, recording fees, and more. Regions Bank will break these down for you, but it’s good to have a general understanding that they exist. It’s like the final flourish on a masterpiece – it costs a little something to get it framed!

So, what’s the takeaway here? If you’re eyeing a 30-year mortgage and considering Regions Bank, you’re on the right track. They offer a solid, reliable product that’s a cornerstone of homeownership for so many. The rates will be influenced by the usual suspects – the economy, the Fed, and your personal financial superpowers.

The most important thing you can do is do your homework. Compare offers from different lenders, talk to loan officers, and understand all the terms and conditions. Don’t be afraid to negotiate. Sometimes, just asking politely can make a difference. And remember, a 30-year mortgage is a commitment, but it’s a commitment that can lead to the joy of owning your own slice of the world, a place to hang your hat, paint your walls whatever color you darn well please, and maybe even build that elaborate pillow fort you’ve always dreamed of.

Ultimately, securing a Regions Bank 30-year mortgage rate is about finding a balance that works for your budget and your dreams. It’s about taking that big leap towards homeownership with a plan in place. And when you finally get those keys in your hand, and you’re standing in your very own home, all the research, the paperwork, and the rate-hunting will feel like a distant, but worthwhile, memory. You’ve got this! Now go forth and find your perfect home!

:max_bytes(150000):strip_icc()/06-09-2023mortgagenews-9ca1a24cc1c7496ebf9909a02ff477de.jpg)

:max_bytes(150000):strip_icc()/July23MortageRatesNews-25-45874d49bd054feb86de585aa2efce03.jpg)