Lying To Get 401k Hardship Withdrawal

:max_bytes(150000):strip_icc()/what-to-know-before-taking-a-401-k-hardship-withdrawal-2388214-v2-211c0d162ae64a95bbe3813f1f9243ad.png)

Let's talk about the 401(k). That magical pot of gold you've been diligently (or maybe not-so-diligently) squirreling away. It's your future self's retirement party fund. But oh, the temptations! Especially when, let's be honest, life throws some curveballs. Suddenly, that nest egg looks less like a future retirement dream and more like a present-day emergency solution.

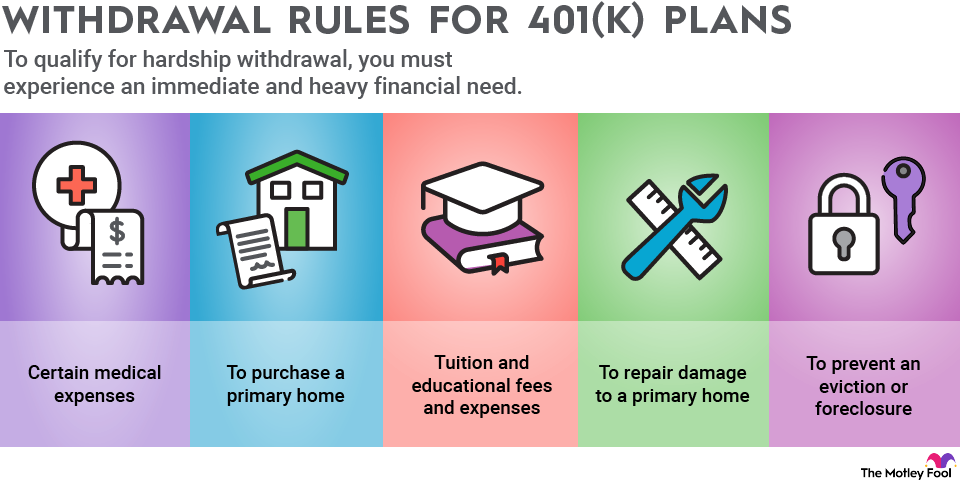

And then there's the hardship withdrawal. Sounds serious, doesn't it? Like you've been shipwrecked on a desert island and this is your only ticket home. The IRS and your employer have this whole system set up, with rules and regulations. They want to make sure you're really in a pickle before you dip into your hard-earned cash.

But sometimes, life's pickles aren't quite the "shipwreck" variety. They're more like... the slightly-too-salty-but-still-edible kind. You know, the kind where you could probably make it work without touching your 401(k), but man, oh man, it would be SO much easier if you could just… you know.

Must Read

And that's where the whispers start. The hushed conversations with friends who have "been there." The late-night internet searches. The gentle, almost artistic bending of the truth. We're not talking about outright fraud here. heavens no! We're talking about... creative interpretation. About framing your situation in the most compelling light possible. Think of it as a dramatic performance, with your 401(k) plan administrator as the esteemed (and slightly oblivious) audience.

Consider the classic "unexpected medical expense." Who among us hasn't had a mysterious rash appear that, while not life-threatening, did require a rather expensive specialist visit? Or perhaps a root canal that, while not an emergency, suddenly became the most pressing issue in your universe? You could say, "Yes, doctor, this pain is excruciating and is severely impacting my ability to concentrate on my financial planning... for retirement."

Then there's the ever-popular "primary residence eviction." Now, maybe your landlord didn't literally hand you an eviction notice. Maybe they just mentioned, in passing, that your rent was going up by a gazillion dollars next month and you should probably start looking. But that's a nuance, right? A detail that might muddy the waters. It’s much cleaner to say, "My home is at risk!" It has a certain urgency, a certain… drama.

We’ve all been there, staring at bills, feeling that familiar knot in our stomach. And the 401(k) just sits there, so close, yet so far. It’s like a siren song, a forbidden fruit. The temptation to just… borrow from future you. Because, let’s face it, future you is probably doing pretty darn well anyway, right? They’ve got their fancy retirement condo and their endless supply of prune juice. They can afford to be a little inconvenienced.

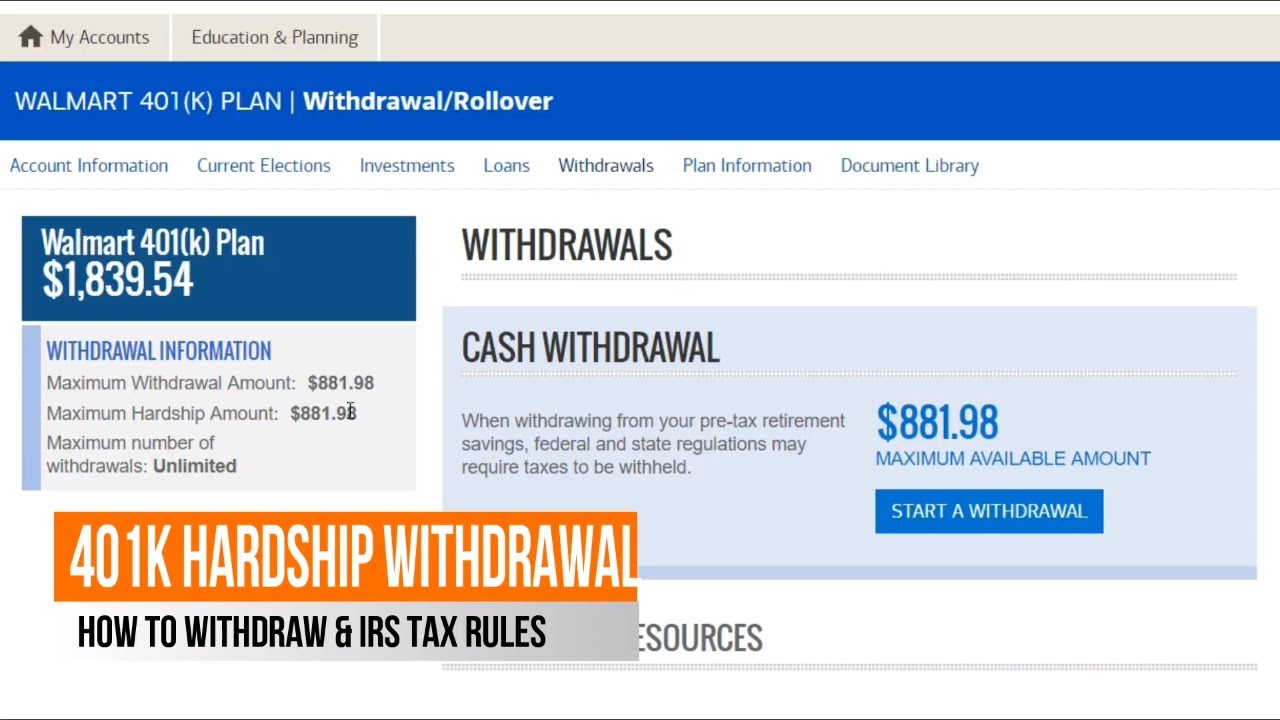

The paperwork for a hardship withdrawal usually involves attesting that you have "no other resources available." This is where the art of omission comes in. Do you have a spare change jar in the back of your car? Technically, that's a resource. But is it a significant resource? Probably not. So, you might just conveniently forget to mention it. It’s not a lie, per se. It’s just… selective memory.

What about that emergency fund you meant to build but never quite got around to? Again, another resource that might have been available if you’d been a bit more organized. But who has time for perfect organization when life is demanding immediate attention? So, you can confidently state that you have no other available resources. You're practically a martyr, bravely sacrificing your present comfort for the vague promise of a future one.

It's a delicate dance, isn't it? You're trying to be honest, but you're also trying to survive. You want to access your money, but you don't want to get in trouble. So, you craft a narrative. You emphasize the pain, the urgency, the sheer necessity of it all. You become a master storyteller, weaving a tale of woe that tugs at the heartstrings of your HR department.

“Sometimes, just a little creative storytelling is all it takes to get your 401(k) to lend a helping hand… in your hour of need.”

And you know what? In a way, it’s kind of brilliant. It’s human nature. We want to protect ourselves, to ensure our immediate well-being. And if a slightly embellished reason is what it takes to access funds that are, ultimately, yours, well, who are we to judge? We’re just trying to keep our heads above water.

Think of it as a small rebellion. A quiet act of defiance against the rigid structures of finance. You're not stealing, you're just... borrowing from yourself, with a little bit of dramatic flair. It's a testament to our ingenuity, our ability to adapt and overcome. And maybe, just maybe, your 401(k) plan administrator secretly admires your moxie. Or perhaps they're just really good at their jobs and have heard it all before. Either way, you got the money. And for now, that's a win. A small, slightly ethically ambiguous, but ultimately victorious win.

![401k Hardship Withdrawals [What You Need To Know] - YouTube](https://i.ytimg.com/vi/AJ0gxuqu6Lw/maxresdefault.jpg)

:max_bytes(150000):strip_icc()/howtotakemoneyoutofa401kplan-79531c969f74433db11c032e3cfd3636.png)