How To Put Your House In A Trust

Hey there! So, you're thinking about your house, huh? That big ol' money pit, or maybe your cozy nest egg. Either way, it's probably one of your most valuable assets. And you're wondering, "Can I, like, safely put it in a trust?" The answer, my friend, is a resounding YES! And guess what? It's not as scary or complicated as it sounds. Think of it like this: it's basically giving your house a fancy, official VIP pass for the future.

Why would you even want to do this, you ask? Well, imagine this: you’ve worked your tail off to buy this place. You’ve painted the walls (probably poorly, let’s be honest), fixed leaky faucets, and maybe even battled a rogue squirrel in the attic. So, you want it to go to the people you care about, right? Without a fuss. Without the probate monster gobbling up your hard-earned equity. Bingo! That’s where trusts come in. They’re like a secret handshake for your stuff.

Let’s ditch the jargon for a sec, okay? A trust, in simple terms, is a legal arrangement where you (the grantor) give your property (your house!) to someone else (the trustee) to hold and manage for the benefit of a third party (the beneficiary). Sounds official, right? But don't let that intimidate you. You can often be all three roles, at least initially. Mind. Blown. 🤯

Must Read

So, how do you actually do this? It's not like you just write "My house belongs to my nephew now!" on a napkin. Although, wouldn't that be a hilarious inheritance story? Nope, we’re talking about a more structured approach. You'll need to create a legal document called a trust agreement. This is where all the magic happens. It outlines who’s who, what’s what, and when things are supposed to go down. Think of it as the instruction manual for your house's future.

The Big Players in Trust Town

Let’s break down these roles, because knowing them is half the battle. Seriously, knowing the names of the characters in your favorite show is easier than this, I promise.

The Grantor (That's You, Superstar!): You’re the one who owns the house, and you’re the one setting up the trust. You’re basically the benevolent dictator of your real estate destiny. You decide all the rules. Pretty cool, huh?

The Trustee (Your House's Guardian Angel): This person (or entity, like a bank) is responsible for managing the property according to the trust's instructions. They’re like the super-responsible friend you trust with your Netflix password. They have to act in the best interest of the beneficiaries. No funny business allowed!

The Beneficiary (The Lucky Ducks!): These are the people who will eventually benefit from the trust. It could be your kids, your grandkids, your favorite charity, or even your incredibly spoiled pet (hey, no judgment here!). They get the goods when you say so.

Now, here’s the kicker: in a revocable living trust, which is super common for house transfers, you can be all three! Yep, you can be the grantor, the trustee, and the beneficiary all at once. You're essentially gifting your house to yourself, but in a way that sets up a smooth transition later. It's like giving yourself a present that your future self will really appreciate. Talk about forward-thinking!

Why Bother? The Actual Benefits (Beyond the Cool Factor)

Okay, so we’ve touched on it, but let’s really dive in. Why would you go through the (minor) hassle of setting up a trust for your house?

Bye-Bye Probate! (Hallelujah!) This is the big one. Probate is that legal process where a court oversees the distribution of your assets after you pass away. It can be a long, expensive, and super public affair. Think of it as a bureaucratic nightmare. Your house, if it’s in a trust, bypasses probate. Poof! Gone. Like a magic trick. Your loved ones get the house faster and with way less drama. Who doesn't love less drama?

Privacy, Please! Wills become public record during probate. That means anyone can go and see what you owned, who you left it to, and how much it was worth. Yikes! A trust, however, is a private document. Your financial life stays… well, your life. Keep those nosy neighbors guessing!

Control, Control, Control! With a trust, you can dictate exactly how and when your beneficiaries receive your house. Maybe you want them to inherit it outright. Or maybe you want them to have it only when they reach a certain age, or when they get married. You can even set conditions! It's like a personalized gift-giving ceremony, but with a house. You're the director of your own real estate movie!

Protection Against Lawsuits and Creditors. Depending on the type of trust and how it's set up, your house can be protected from certain creditors or lawsuits. This is a bit more complex and definitely something to discuss with a legal pro, but it's a powerful benefit!

Planning for Incapacity. What happens if you become unable to manage your affairs? If your house is in a living trust, your successor trustee can step in seamlessly and manage it for you without the need for a court-appointed conservator. It's like having a reliable backup system in place. Your house stays safe and sound.

The "How-To" Walkthrough (It's Not Rocket Science!)

Alright, let's get down to the nitty-gritty. How do you actually make this happen? Grab your favorite beverage, because here we go!

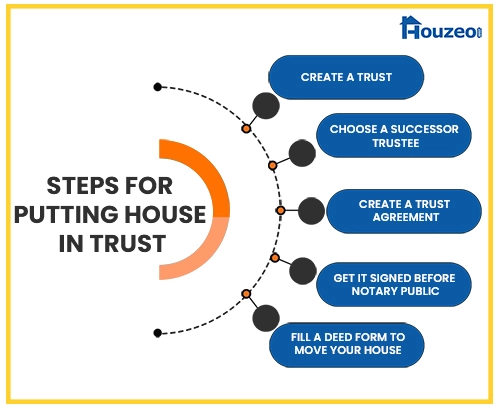

Step 1: Decide What Kind of Trust You Need.

As mentioned, a revocable living trust is the most common choice for homeowners looking to avoid probate. It’s called "revocable" because you can change it or even cancel it while you’re alive. "Living" means it’s created and operates while you’re still kicking. Easy peasy.

There are other types, like irrevocable trusts, but those are usually for more complex situations and generally shouldn't be changed. For just getting your house in order, a revocable living trust is probably your jam.

Step 2: Get Your Paperwork in Order.

This is where things get official. You'll need to draft a trust agreement. This is the document that names the grantor, trustee(s), and beneficiary(ies), and outlines all the rules and provisions for your house. Think of it as the constitution for your house's trust life.

Pro Tip: While you can find online templates, for something as significant as your home, it's highly recommended to work with an experienced estate planning attorney. They know all the legal mumbo-jumbo, can make sure it’s done correctly, and tailor it to your specific situation. It’s an investment in peace of mind, trust me. You don't want to mess this up!

Step 3: Fund the Trust (This is the Big Move!).

This is the crucial step where you actually transfer ownership of your house to the trust. It’s not enough to just have the trust document. You have to officially change the deed to your property. This usually involves preparing a new deed (often a quitclaim deed or warranty deed) that transfers the property from your name to the name of the trust. For example, instead of "John Doe," it will read "John Doe, Trustee of the John Doe Revocable Living Trust."

This deed then needs to be signed, notarized, and recorded with your local county recorder's office. This is the official "Hello, Trust! Welcome to the family!" moment for your house. Don't skip this! It’s like buying a car but forgetting to get the keys. Useless!

Step 4: Appoint Your Successor Trustee(s).

This is the "what if" plan. Who takes over as trustee if you can no longer serve? This could be a spouse, a child, a trusted friend, or even a professional trustee. You'll name them in your trust agreement. Make sure you talk to them beforehand! Don't just surprise your cousin Mildred with the responsibility of managing your multi-million dollar mansion. Unless she's secretly a real estate mogul, then maybe.

Step 5: Update Your Beneficiary Designations.

While your house is now in the trust, you might have other assets like bank accounts or life insurance policies. Make sure those beneficiary designations align with your overall estate plan. It’s all about making sure everything flows together like a well-choreographed dance.

A Few Things to Keep in Mind (The "Don't Forget This!" Section)

Taxes: For a revocable living trust, there generally aren't immediate tax implications when you transfer your house. You'll still pay property taxes and any other usual taxes associated with homeownership. The tax benefits usually come into play later, depending on your overall estate and how it’s structured. Again, talk to a tax professional or your attorney about this!

Mortgages: If you have a mortgage on your house, transferring it to a trust might trigger the "due-on-sale" clause in your mortgage agreement. However, there are often exceptions for transfers to living trusts where you are the primary beneficiary. Your mortgage lender might need to be notified. It's best to check with your lender and your attorney on this. Don't let this be a surprise!

It’s Not Just for the Rich and Famous: Seriously, anyone can benefit from putting their house in a trust. It’s about protecting your assets and ensuring your wishes are carried out. Don't let the fancy lawyers or the Hollywood portrayals fool you. This is practical stuff for real people.

Consistency is Key: Once your house is in the trust, make sure all related documents and actions reflect that. If you’re selling the house later, the trust will be the seller, not you personally. It’s about maintaining that consistent legal identity for your property.

Review and Update: Life happens! Your family situation might change, your wishes might evolve. Periodically review your trust agreement with your attorney to make sure it still reflects your current intentions. It’s not a set-it-and-forget-it kind of deal.

So, there you have it! Putting your house in a trust might sound a little intimidating at first, but with a little guidance and a good attorney, it’s a totally manageable process. It's like giving your house a superhero cape for the future, protecting it and ensuring it gets to where you want it to go, without all the messy drama. Go forth and empower your property!