How To Get Prequalified For Affirm

You know that feeling, right? You’re scrolling through a cool online store, you’ve found the thing – that ridiculously comfy sweater, that gadget you’ve been eyeing for months, or maybe even something more substantial like new furniture for your apartment. Your finger hovers over the “Add to Cart” button, but then… the price tag. Suddenly, that immediate gratification feels a little out of reach. It’s like seeing your dream car parked just a little too far away. You sigh, maybe add it to your wishlist, and continue browsing, a tiny bit of disappointment settling in. Sound familiar? Yeah, me too. I remember a while back, I was desperate for a new espresso machine. Mine had officially given up the ghost, and my mornings were… well, let’s just say they were less than caffeinated and significantly more grumpy. I found the perfect one online, sleek, shiny, and promising lattes that would make my taste buds sing. But the price? Oof. It was a bit more than my immediate budget allowed. I almost resigned myself to instant coffee forever.

Then, I remembered something. A little whisper of a payment option that had been popping up on more and more sites. Affirm. I’d seen it before, tucked away near the checkout, but hadn't really paid it much mind. Was it just another one of those credit card things I already had too many of? Or was it something… different? Curiosity, and the desperate need for a decent cappuccino, got the better of me. I decided to dive in and see what this “Prequalify” business was all about. And honestly? It was way less scary than I thought.

So, What’s the Deal with Affirm Prequalification?

Alright, let’s cut to the chase. You’re probably wondering, “Okay, story time is nice, but how does this actually work?” Think of prequalification as a friendly handshake with Affirm, not a full-blown wedding proposal. It’s their way of saying, "Hey, based on some quick checks, we think you might be able to borrow X amount of money from us for your purchase." It's a super low-commitment way to see if you can actually afford that thing you’ve been dreaming about without messing with your credit score too much. Pretty neat, huh?

Must Read

This is important because, let’s be honest, the idea of taking on any kind of new financing can feel a bit daunting. We’ve all heard the horror stories, or maybe even lived through them, where a simple purchase turned into a debt trap. So, the fact that Affirm has this prequalification step? It’s a huge win for peace of mind. You’re not signing your life away; you’re just getting a ballpark figure.

The “Soft” Touch: Why Prequalification is Your Friend

Here’s the magic trick, and it’s a good one: prequalification usually involves a “soft” credit pull. What does that mean? Imagine a gentle breeze versus a strong gust of wind. A soft pull is like that breeze. It’s a check of your credit report that doesn’t negatively impact your credit score. This is a big deal. You know how applying for a new credit card or loan often shows up on your credit report as a “hard inquiry” and can ding your score a few points? Yeah, not with this. Affirm does this so you can shop around and see your options without the penalty. It’s like window shopping for financing, and it’s totally guilt-free!

So, when you go through the prequalification process, you can be pretty confident that it won't hurt your credit score. This means you can explore your options with Affirm at different retailers, or even just to see what you might qualify for, without worrying about damaging your financial reputation. It’s a smart move for anyone who’s looking to make a purchase but wants to understand their payment flexibility first.

Ready to Take the Plunge? Here’s How to Prequalify

Okay, so you’re convinced. You want to see if that espresso machine (or whatever your current obsession is) can be yours without emptying your bank account in one go. The good news is, it’s usually a pretty straightforward process. Think of it like filling out a quick online form, but instead of asking for your favorite color, it’s asking for a few key details.

Step 1: Find a Retailer That Uses Affirm.

This is your starting point. Affirm partners with a ton of online retailers, from big names in electronics and furniture to smaller boutiques and even travel companies. You’ll usually see the Affirm logo displayed prominently, often near the product price or as a payment option at checkout. So, when you’re on a website and you see that familiar Affirm logo, that’s your cue. Click around a bit, see if there’s a specific “Learn More” or “Prequalify” link, or sometimes, it’s just a direct option during the checkout process.

Step 2: Look for the Prequalification Option.

Once you've found a retailer and an item you like, the next step is to locate the prequalification button or link. This can vary slightly from site to site. Sometimes, it’s right on the product page, a little button that says “Check your payment options” or “Prequalify for financing.” Other times, you might only see the option once you’ve added the item to your cart and proceeded to checkout. Don’t panic if you don’t see it immediately; it’s often just a click or two away. It’s like searching for a hidden gem on a treasure map!

Step 3: Fill Out the Quick Application.

This is where the “handshake” happens. You’ll be taken to a secure Affirm page (or a pop-up within the retailer’s site). They’ll ask for some basic information. We’re talking things like:

- Your Name

- Email Address

- Phone Number

- Date of Birth

- The last four digits of your Social Security Number (SSN)

Now, I know what you might be thinking. “My SSN? Isn’t that a bit much for just prequalification?” It’s understandable to be cautious! But remember, this is for a financial product. They need a way to identify you and check your creditworthiness. Affirm uses this information for that soft credit pull I mentioned. It’s a standard practice for financial services. Just make sure you’re on a legitimate Affirm page or a secure pop-up from the retailer – look for the padlock icon in your browser’s address bar. Always a good habit!

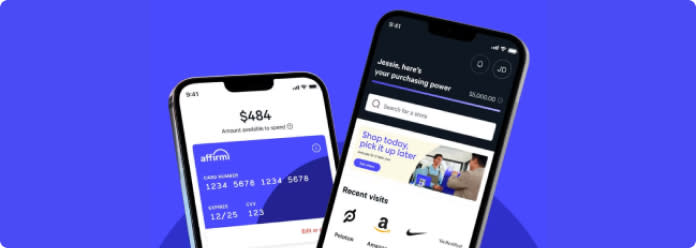

Step 4: Receive Your Prequalified Offer (Almost Instantly!).

This is the exciting part! After you submit your information, Affirm will do its magic behind the scenes. Within seconds, you should see your prequalified offer. This will typically include:

- The maximum amount you’re approved to borrow.

- The different payment plan options available to you, which might include different lengths of time (e.g., 3, 6, 12 months) and the associated interest rates (or sometimes, 0% APR if you’re lucky and the retailer offers it!).

- Your estimated monthly payment for each option.

It’s like getting a personalized menu of payment options, so you can choose the one that best fits your budget. No more guessing games!

What Happens After Prequalification?

So, you’ve got your offer. What now? This is where you get to be the boss of your purchase. You’re not obligated to do anything!

Option A: You Like What You See (and Can Afford It!)

Hooray! If the prequalified offer works for you, and you’re ready to make that purchase, you can proceed with selecting your Affirm payment plan right there. You’ll likely need to provide a bit more information for the final approval, like your address and potentially your full SSN, and then you’ll complete the purchase. You’ll then receive a confirmation of your loan details and payment schedule.

It’s at this stage, when you’re committing to a loan, that Affirm will perform a hard credit check. This is standard for any loan or credit line. However, since you’ve already seen your prequalified offer, you’ll have a good idea of what to expect, and you won’t be surprised by a hard inquiry. Think of it as the final step before you get your hands on that coveted item!

Option B: Not Quite Right (Yet?)

No worries! This is the beauty of prequalification. If the amounts aren’t what you hoped for, or the payment plans don’t quite fit your budget, you can simply close the window. You haven’t committed to anything, and your credit score remains untouched. You can go back to browsing, save up a bit more, or look for other financing options. The world (and your wishlist) is still your oyster!

It’s important to remember that prequalification is an estimate. The final approval amount can sometimes vary slightly, but it gives you a very strong indication of what you can expect. So, don’t feel pressured if it’s not perfect the first time. You can always try again later or explore other options.

Who Is Affirm Prequalification For?

Honestly? Pretty much anyone who’s ever looked at a price tag and thought, “If only…”

- The Budget-Conscious Shopper: If you like to plan your finances and avoid overspending, prequalification lets you know exactly what you can afford before you commit.

- The Instant Gratification Seeker (with a sensible side): You want it now, but you also want to pay for it responsibly. Prequalification bridges that gap.

- The Credit-Conscious Explorer: You want to understand your financing options without the fear of damaging your credit score.

- Anyone Making a Larger Purchase: Think furniture, electronics, appliances, or even that dream vacation. Spreading out the cost can make these big-ticket items much more manageable.

It’s really for anyone who values transparency and wants to make informed financial decisions. It takes away a lot of the guesswork and anxiety that can come with making larger purchases online.

A Few Extra Tips for Navigating Affirm

Before you go running off to prequalify for everything on your wishlist (tempting, I know!), here are a few things to keep in mind:

- Check for 0% APR Offers: Many retailers partner with Affirm to offer 0% interest on certain payment plans, especially for specific promotions or purchase amounts. If you can snag one of these, you’re essentially getting an interest-free loan, which is amazing!

- Read the Fine Print: Always understand the terms of your loan, including the interest rate, payment schedule, and any potential late fees. Affirm is generally transparent, but it’s your responsibility to know what you’re agreeing to.

- Prequalification is Not a Guarantee: While it’s a very strong indicator, the final approval can sometimes differ. Be prepared for that small possibility.

- Be Mindful of Your Limits: Just because you can prequalify for a certain amount doesn’t mean you should borrow it. Only borrow what you can comfortably repay. This is about making purchases easier, not about getting into debt.

So, there you have it! Getting prequalified for Affirm is a simple, smart, and low-risk way to explore your payment options for those purchases that make your heart (and your wallet) sing. It’s like having a personal shopper for your finances, helping you figure out how to get that thing you want without the immediate financial stress. Now, if you’ll excuse me, I have a certain espresso machine that’s just waiting for me to finish this article so I can finally place my order. Happy shopping (and happy prequalifying)!

.png?format=1500w)