How To Avoid Paying Tax On Pension Drawdown

So, picture this: my Uncle Barry, bless his cotton socks, finally decided to dip into his pension pot. After decades of diligent saving, he was ready for that Hawaiian shirt and a piña colada lifestyle. He calls me up, all excited, talking about the cruise he's booked, the new set of golf clubs he's eyeing. Then, the bombshell. "They're taking a chunk out of it, you know," he says, his voice suddenly deflated. "The taxman. Can you believe it?" Barry, my dear Barry, was operating under the blissful illusion that his hard-earned pension money was somehow exempt from the prying eyes of HMRC. Oh, the innocence!

And that, my friends, is where we start our little chat today. Because Barry’s not alone. Many of us, as we get closer to that magical retirement age, start thinking about accessing our pension, not necessarily about the tax implications of accessing it. It’s a bit like planning your epic vacation without checking your passport expiry date, isn’t it? You’ve got the tickets, you've got the itinerary, but then… oh dear.

The truth is, when you start drawing an income from your defined contribution pension (that's the more common pot you’ve built up over the years), HMRC does expect its fair share. It's not exactly a secret, but it’s also not exactly plastered on the front page of the Daily Mail. So, how do we navigate this potentially thorny issue? Can we, dare I say it, minimise the tax we pay on our pension drawdown? The short answer is yes, but it requires a bit of planning and, frankly, a sprinkle of cleverness.

Must Read

The Dreaded Income Tax: Why It's There and Why It Feels So Unfair

Let’s get this out of the way first. When you take money out of your pension pot as income, it's generally treated as taxable income by HMRC. This means it gets added to any other income you might have in that tax year (like state pension, or income from any part-time work you’re still doing) and taxed at your marginal rate. So, if you're a basic rate taxpayer, you'll pay 20% on that pension income. Higher rate? That's 40%. And the additional rate payers, well, you know the drill.

It does feel a bit like a double whammy, doesn't it? You paid tax on the money before it went into your pension (in the form of tax relief on your contributions), and now you're paying tax on it again when you take it out. It’s enough to make you want to go back to work just to avoid the whole palaver! But hold your horses. There are legitimate ways to manage this.

Understanding Your Tax-Free Entitlement: The Golden Ticket

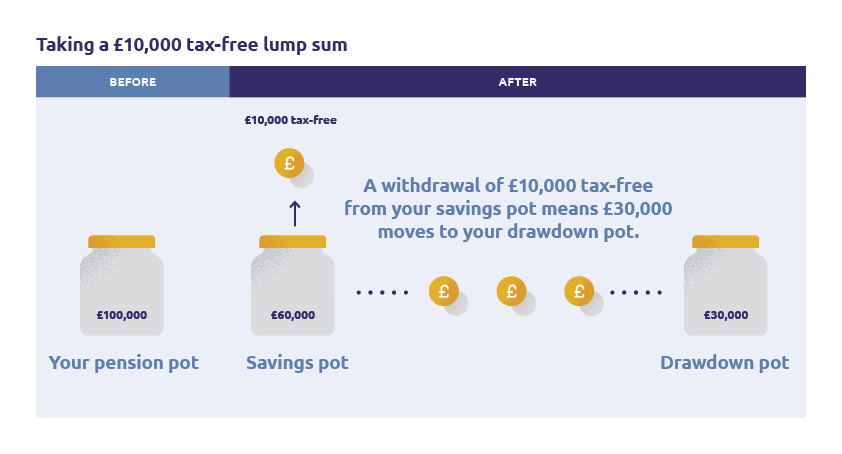

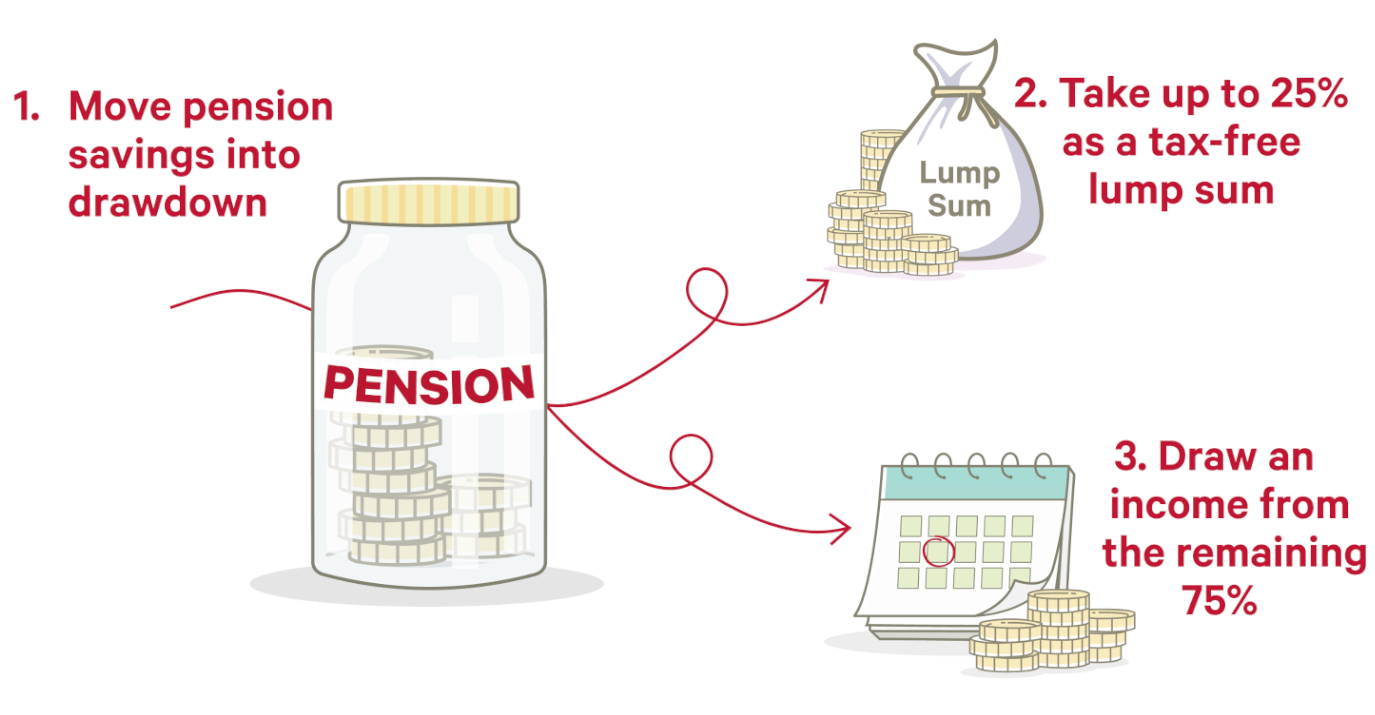

Here’s the first ray of sunshine. When you access your defined contribution pension, you’re usually entitled to take 25% of your pension pot as a tax-free lump sum. This is often referred to as the Pension Commencement Lump Sum (PCLS). This is pure, unadulterated, tax-free cash. Hallelujah!

So, if you have a £200,000 pension pot, you can take £50,000 of that completely tax-free. Poof! Gone. No questions asked by HMRC. This is your first and arguably most powerful tool for reducing your taxable pension income.

Top tip: Make sure you claim this. Don't just let it sit there because you're not sure how it works. Your pension provider will guide you through it, but it's essential to understand you have this entitlement. Think of it as your retirement 'rainy day' fund, or your 'treat yourself' fund, without any tax headaches.

The Art of Strategic Income Withdrawal: Don't Just Grab It All

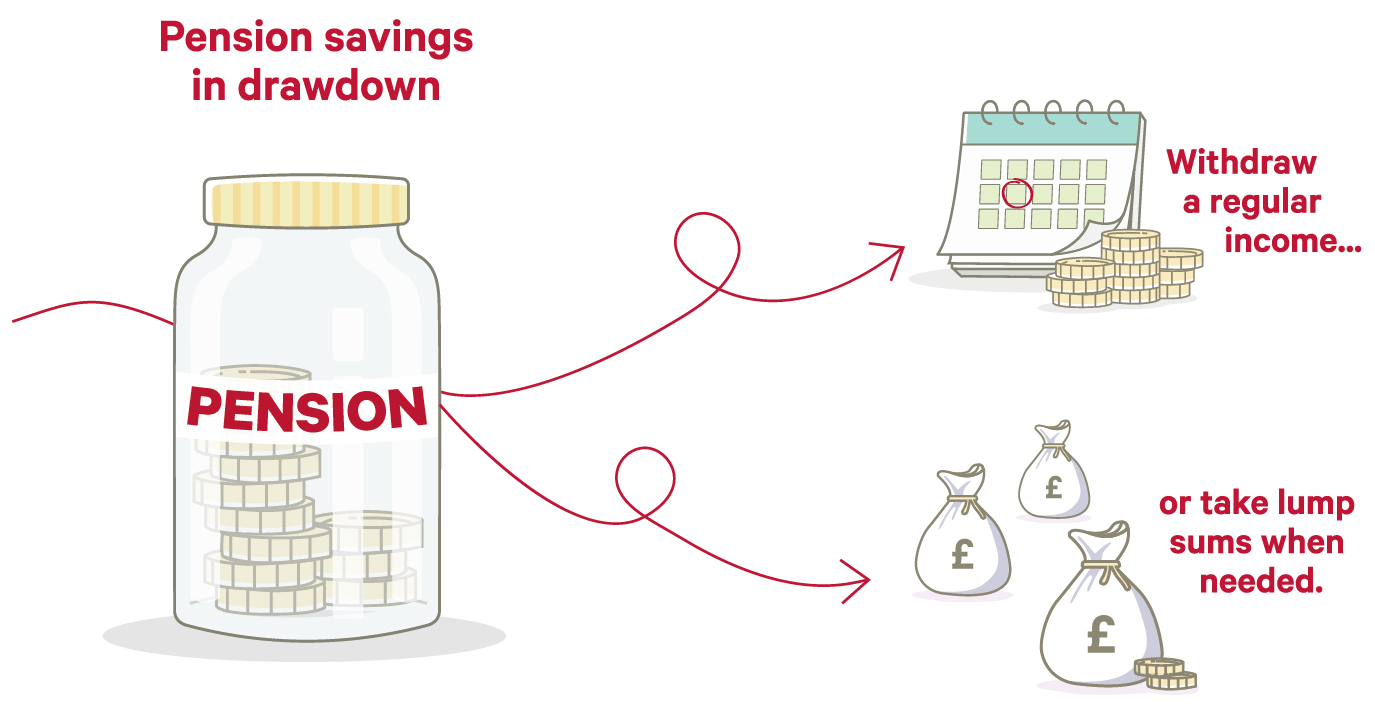

This is where Uncle Barry might have stumbled. He probably thought, "Right, I'm retired, I need money, so I'll just take out X amount each month." But the way you take that income makes a huge difference. This is where "pension drawdown" (or more accurately, "flexi-access drawdown") comes into play.

Flexi-access drawdown allows you to keep your pension pot invested and draw an income from it as and when you need it. Unlike annuity products, where you exchange your pot for a guaranteed income for life, drawdown gives you flexibility. And with flexibility comes responsibility… and opportunity!

The key here is to be strategic with your withdrawal amounts. Instead of taking a fixed, larger sum that pushes you into a higher tax bracket, consider taking smaller, more manageable amounts. This can be especially effective in years when you might have other, lower-taxable income, or in years where you have fewer expenses.

Leveraging the Personal Allowance: Your Tax Shield

Everyone in the UK has a personal allowance – the amount of income you can earn before paying income tax. For the 2023/2024 tax year, this is £12,570. This allowance resets every year.

If your total taxable income for the year (including your state pension and any pension drawdown income) falls within your personal allowance, you won't pay any income tax on it. This is gold, pure gold! So, if your annual pension drawdown income is, say, £10,000, and you have no other significant income, you’re laughing. You’ve effectively drawn £10,000 from your pension and paid £0 in tax on it.

Now, imagine you need more than that. Instead of taking a lump sum that blows past your personal allowance, you can stagger your withdrawals. For instance, if you need £20,000 in a year, and your personal allowance is £12,570, you could aim to draw around £10,000 from your pension. This would leave you with £2,570 of your personal allowance unused, and you'd pay tax on the remaining £10,000 of pension income. But if you took £20,000, you'd pay tax on the full £20,000. See the difference?

This requires a bit of juggling. You need to keep an eye on your total annual income and plan your withdrawals accordingly. It's like being a conductor of your own financial orchestra, ensuring each instrument (your income streams) plays at the right volume.

The Marriage Allowance: A Tiny Boost for Some

This one’s a bit niche, but worth mentioning if it applies to you. If you’re married or in a civil partnership, and one of you earns less than the personal allowance (£12,570) and the other is a basic rate taxpayer, you might be able to transfer 10% of the unused personal allowance to your partner. This can give you a tax saving of up to £252 a year.

How does this relate to pensions? Well, if one partner is drawing a significant pension income and pushing them into a higher tax bracket, while the other has little to no income, applying the Marriage Allowance could slightly reduce the overall tax burden on their combined income. It’s a small saving, but every little bit counts, right? Especially when it comes to taxes!

Timing is Everything: The Tax Year Advantage

The UK tax year runs from April 6th to April 5th. This might seem like a trivial detail, but it’s crucial for tax planning. When you're managing your pension drawdown, you can be smart about when you take your income.

Let’s say you've had a year where you’ve had some unexpected expenses, or perhaps you’ve been doing a bit of freelance work. Your taxable income might be higher than usual. In this scenario, you might choose to take less pension income during that tax year and more in the next, provided your needs allow. Conversely, if you know you’ll have a quiet year financially, you might take a larger pension income to take advantage of your full personal allowance.

This flexibility is one of the biggest advantages of flexi-access drawdown. You're not locked into a rigid system. You can adapt your withdrawals based on your circumstances and the tax year. It’s about being proactive, not reactive.

Pensions and Other Income: The Holy Grail of Tax Efficiency

This is where things get really interesting, and where you can achieve significant tax savings. If you have multiple sources of income in retirement, you can use them strategically to minimise your tax bill.

State Pension: Your Baseline Income

Most people will receive a State Pension. This is taxable income. So, when you calculate your total income for tax purposes, don't forget to include this. Often, the State Pension alone is well within the personal allowance, meaning it’s tax-free for many. If your State Pension does push you over the personal allowance, then any subsequent pension drawdown income you take will start being taxed.

Rental Income: A Taxable Beast (But Manageable)

Some people retire and then draw an income from properties they own. Rental income is taxable. The good news is that you can deduct certain expenses against your rental income (like repairs, mortgage interest, and letting agent fees) before tax is calculated. This can reduce your taxable rental income. However, if you have substantial rental income, it could push you into higher tax brackets, affecting how much tax you pay on your pension drawdown.

The strategy here is to try and balance these income streams. If your rental income is high in one year, you might take less pension income. If your rental income is low, you might draw more from your pension, as long as you’re still within your personal allowance or paying tax at a rate you’re comfortable with.

Investments Outside Pensions: Capital Gains Tax and Dividends

Many retirees will have ISAs (Individual Savings Accounts), which are tax-free. They might also have other investment accounts. Income from these can be in the form of dividends or capital gains.

Dividends have their own tax allowance (£1,000 for 2023/2024) and then are taxed at different rates depending on your income tax band. Capital gains also have an annual exempt amount (£6,000 for 2023/2024) before tax is applied. These allowances also reset each year.

This is where you can get really clever. If you’ve already used up your personal allowance with your State Pension and pension drawdown income, and you’re looking for additional income, you might draw dividends from an investment account. This income might be taxed at lower rates than your pension income would be if you drew more.

Conversely, if you're only drawing a small amount from your pension and staying within your personal allowance, you can then start drawing from your ISAs or crystallising capital gains tax allowances, knowing that your pension income isn't pushing you into higher tax brackets.

Think of it like this: Your pension drawdown is your primary income, but your ISA and other investments are your secondary and tertiary income streams. You can arrange these streams so that the water flowing from the lower ones (ISAs) is less taxed, or untaxed, and you only let the higher ones (pension drawdown) flow enough to fill your needs without overflowing into higher tax bands.

![Avoiding Tax on Pensions: What Pensioners Need to Know [2025]](https://d269azu04l8n6x.cloudfront.net/wp-content/uploads/2025/01/avoid-paying-tax-on-your-pension-768x512.jpg)

The Role of a Financial Adviser: Don't Be Afraid to Ask for Help!

Now, I know what you might be thinking. "This is all very well, but it sounds complicated. I don't want to mess it up!" And you're absolutely right. This isn't simple stuff. There are rules, allowances, and potential pitfalls.

This is precisely why so many people turn to qualified financial advisers. They are trained to understand the complexities of the tax system and pension rules. They can look at your entire financial picture – your pension pot size, other income sources, your spending needs, your risk tolerance – and help you create a bespoke withdrawal strategy.

They can tell you the best way to take that 25% tax-free lump sum, how to phase your income withdrawals, when to draw from different pots, and how to make the most of tax allowances. For many, the fee they pay for advice is more than offset by the tax savings they achieve.

It’s not about trying to evade tax; it’s about legitimately reducing your tax liability by making informed decisions. It’s about being tax-efficient. Uncle Barry might have benefited from a chat with an adviser before he booked that cruise, just saying!

A Final Thought on Inheritance Tax

While we're talking about pensions and drawing them down, it's worth a brief mention of what happens when you pass away. If you die before age 75, your remaining pension pot is usually tax-free for your beneficiaries, regardless of how you’ve drawn from it. If you die after 75, your beneficiaries will pay income tax at their marginal rate on any income they receive from the remaining pot.

This isn't directly about avoiding tax on your drawdown, but it's a crucial part of pension planning. Making sure your pension pot is structured in a way that benefits your loved ones efficiently is another layer of financial strategy.

So, can you avoid paying tax on pension drawdown? Well, you can't avoid it entirely if you need to draw more than your tax-free lump sum and personal allowance. But you can absolutely minimise it. By understanding your tax-free entitlements, planning your withdrawals strategically, leveraging your personal allowance, and coordinating with other income sources, you can keep more of your hard-earned retirement money. And who wouldn't want that? Now, go forth and be tax-smart!