How Much You Should Spend On A Car

Alright, pull up a chair, grab your latte (or your suspiciously strong instant coffee, no judgment here), and let's talk about the four-wheeled beast that lives in your driveway, or perhaps, a distant, unattainable dream. We're diving headfirst into the wonderfully murky waters of how much dough you should actually be shelling out for a car. And let's be honest, for most of us, this isn't a casual "ooh, that one's shiny!" decision. It's more of a "will I be eating ramen for the next decade?" existential crisis.

So, picture this: you're at the dealership, the fluorescent lights are blinding, the salesperson is doing that thing with their eyebrows that implies they've known you since kindergarten and therefore know exactly what your soul craves. You're eyeing that sleek sedan that looks like it could outrun a cheetah, or maybe that monstrous SUV that can probably double as a small apartment. The question looms: what's the magic number?

The "Just Because It Has Four Wheels Doesn't Mean It Owns You" Rule

First off, let's ditch the idea that you need a car that costs more than your entire life savings, plus a kidney. Unless you're a Formula 1 driver who can actually use those aerodynamic spoilers, or you plan on hauling your entire extended family, including their pet llamas, on a regular basis, you probably don't need that souped-up sports car that guzzles gas like a thirsty marathon runner.

Must Read

Think about it. Your car is essentially a very expensive metal box that gets you from Point A to Point B. Sure, it can have heated seats that feel like a hug from a fluffy cloud, and a sound system that could theoretically trigger seismic activity, but at its core, it's a utility. And utilities, my friends, should not bankrupt you. I mean, I once saw a guy paying for his car with bags of loose change. Bags! Let's try to avoid that particular scene.

The "Don't Let Your Car Become Your Boss" Doctrine

This is where things get serious. The biggest mistake people make is buying a car that's simply too much car. We're talking about monthly payments that make your eyes water, insurance premiums that could fund a small nation's space program, and fuel costs that would make a Saudi prince blush. When your car dictates your entire financial life, it's no longer your servant; it's your overlord. And nobody wants to be ruled by a Honda Civic, no matter how reliable it is.

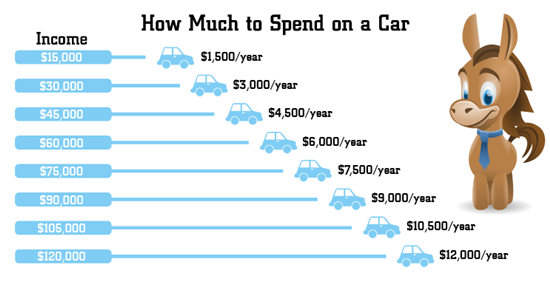

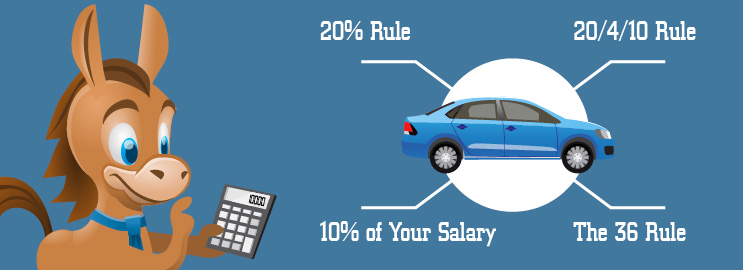

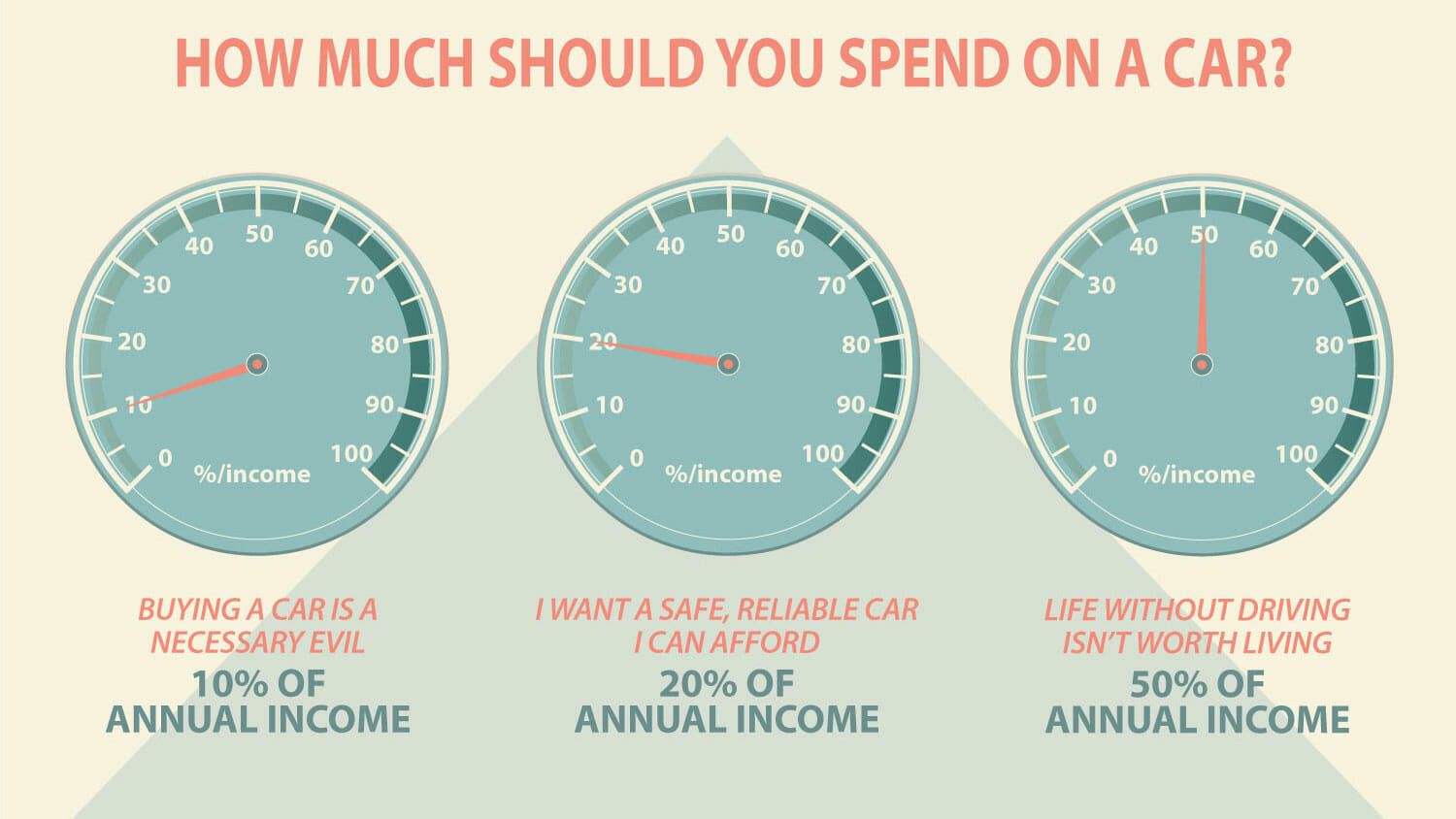

A good rule of thumb, and this is where the actual advice sneaks in, is the 20/4/10 rule. Sounds like a secret handshake, right? Well, it's almost as cool. It means putting down at least 20% for your down payment. Why? To avoid owing more than the car is worth the second you drive it off the lot (that magical depreciation, folks!). Second, aim for a loan term of no more than 4 years. Shorter loan, less interest paid. Boom! Your wallet thanks you. And finally, your total monthly vehicle expenses (loan payment, insurance, gas, maintenance) should not exceed 10% of your gross monthly income.

Now, let's be real. That 10% can feel like a tiny sliver of pie in some cities. If you live in a place where parking costs more than your rent, or where your commute involves navigating a labyrinth of potholes the size of small swimming pools, that 10% might need a slight adjustment. But the principle remains: don't let your car consume your disposable income like a ravenous Pac-Man.

The "What's Your Actual Driving Life Like?" Interrogation

Let's get brutally honest here. Do you really need that giant SUV if your daily commute is a thrilling 10-mile journey to the grocery store and back? Are you regularly scaling Mount Everest with your car, or are you mostly stuck in rush hour traffic, contemplating the deeper meaning of life and the questionable music choices of other drivers?

Consider your lifestyle. If you're a solo city dweller who occasionally goes on weekend trips, a zippy compact or a small crossover might be your best friend. It'll be easier to park, cheaper to fuel, and probably won't give you a complex every time you see a gas station. If you're a suburban parent wrangling a brood of energetic offspring and a week's worth of groceries, a minivan or a larger SUV might be a legitimate necessity. Though, a minivan, in my humble opinion, is the unsung hero of the automotive world. It's basically a mobile command center with cup holders. What's not to love?

And for the adventurers out there, the ones who dream of off-roading and escaping the mundane? Sure, a capable 4x4 might be in your cards. But ask yourself: how often will you actually use that feature? Be honest. We've all bought things for our hobbies that ended up gathering dust, haven't we? Your car can be the same way. Don't buy an off-road beast if your most daring adventure involves navigating a particularly challenging speed bump.

The "Depreciation: The Silent Car Killer" Lecture

Here's a fun fact: the moment you drive a brand-new car off the lot, it loses a significant chunk of its value. It's like buying a fancy cake, taking one bite, and then realizing you have to sell it for half price. Tragic, I know. New cars can depreciate by as much as 20% in the first year alone. That's more than some people's entire annual salary!

This is why pre-owned cars often make a lot more sense. You're letting someone else take that initial depreciation hit. Think of it as a public service. You're saving money by allowing another human being to go through that painful first-year drop in value. And with certified pre-owned programs and thorough inspections, you can often get a car that's practically new without the new-car price tag. It's a win-win, folks!

Of course, there's a sweet spot. A car that's 2-3 years old often offers the best of both worlds: most of the depreciation has already happened, and it's still relatively modern and reliable. Avoid cars that are too old, though. Because while a vintage beauty can be charming, a 15-year-old car with 200,000 miles might just become your personal mechanic shop. And nobody wants that kind of commitment.

The "Hidden Costs of Car Ownership" Conspiracy

Beyond the sticker price and the monthly payment, there's a whole ecosystem of costs that can sneak up on you. We're talking about insurance, which can vary wildly depending on your age, driving record, where you live, and the type of car you drive. That sporty convertible might look cool, but its insurance premium might make you want to trade it in for a bicycle.

Then there's maintenance. Oil changes, tire rotations, brake jobs – these are the inevitable tune-ups that keep your metallic steed chugging along. Some cars are notoriously cheaper to maintain than others. Do your research! A car that requires obscure, hard-to-find parts can quickly turn a small repair into a wallet-emptying saga. I once heard of a guy who had to sell his prized vintage car because a single headlight bulb cost more than his rent. True story. (Okay, maybe slightly exaggerated, but you get the point).

And let's not forget fuel. Depending on your commute and the car's fuel efficiency, this can be a significant monthly expense. If you're doing a lot of driving, a car with excellent MPG (miles per gallon) can save you a small fortune over time. Think of it as a long-term investment in your financial well-being. Every time you pass a gas station without grimacing, you've won.

So, What's the Verdict?

The truth is, there's no one-size-fits-all answer. The amount you should spend on a car is as unique as your fingerprint, or your questionable taste in music. It's a delicate balance of your needs, your wants, and most importantly, your financial reality.

Start by honestly assessing your budget. How much can you comfortably afford for a down payment? What monthly payment can you handle without breaking a sweat? And remember to factor in all those pesky hidden costs: insurance, fuel, and maintenance. Don't be afraid to walk away from a deal that feels too good to be true, or conversely, one that feels like a financial straitjacket. Your future self, who is hopefully not living in a cardboard box because of your car, will thank you.

Ultimately, the goal is to find a car that serves you, not the other way around. A car that gets you where you need to go, safely and reliably, without turning you into a financial zombie. So, go forth, do your research, be realistic, and happy car hunting!

:max_bytes(150000):strip_icc()/how-much-should-i-spend-on-a-car-5187853-Final-87443d24566b4badb1cbe262ed1643a8.jpg)