How Much To Spend On A Car

Hey there, car shoppers and dreamers! Ever find yourself staring at those shiny showroom floors, or scrolling through endless online listings, and that little voice in your head starts whispering, "So, uh... how much should I be spending on this thing?" Yeah, me too. It's like trying to pick the perfect ice cream flavor at a shop with a hundred options – exciting, but also a tad overwhelming.

This isn't about fancy math or secret financial wizards. This is about figuring out what makes sense for you, the person who needs to get to work, pick up the kids, maybe escape for a weekend adventure, or just grab that much-needed gallon of milk. Think of it like choosing the right pair of shoes. You wouldn't buy stilettos for a marathon, and you probably wouldn't buy hiking boots for a fancy dinner, right? Your car is kinda the same – it needs to fit your life.

So, let's ditch the jargon and chat about making smart, happy choices when it comes to your next set of wheels. Because, let's be honest, a car is a big deal! It’s not just a metal box; it’s your trusty sidekick, your mobile office, your adventure mobile. And nobody wants their sidekick to be a constant source of financial stress. Wouldn't it be nice if your car brought a smile to your face, not a frown to your bank account?

Must Read

The "What's My Life Like?" Check

Before we even think about dollar signs, let's do a little life audit. Picture your typical week. Are you a daily commuter, battling rush hour traffic for hours on end? Or are you more of a weekend warrior, using your car for short trips to the farmer's market and occasional road trips?

Imagine Sarah, who lives in the city and takes public transport 90% of the time. Her car is mostly for those occasional IKEA trips or visiting her parents across town. For Sarah, a flashy, gas-guzzling SUV would be like buying a speedboat to cross a paddling pool – a bit overkill and expensive to maintain. She probably needs something compact, fuel-efficient, and easy to park.

Now, think about Mark. He lives in a more rural area and has a long commute to his job. He also loves taking his dog to the national park on weekends. Mark needs something reliable, comfortable for long drives, and maybe with a bit more cargo space. His needs are totally different from Sarah's!

This is the first and most important step. Be honest with yourself about your actual needs. Don't get swayed by what your neighbor has or what looks cool in a magazine. What does your life actually demand from a car?

Beyond the Sticker Price: The True Cost of Ownership

Here’s where things get really interesting, and where many people get a little sticker shock. The price you see on the window isn't the whole story. It's like looking at a delicious cake and only considering the price of the flour. You’re missing out on the butter, the sugar, the frosting, and the baker’s time!

We're talking about things like:

- Fuel costs: Do you want to be a regular at the gas station, or do you prefer to wave goodbye to the pump more often? Think about your daily mileage and the car's fuel efficiency (miles per gallon or MPG). A car that sips gas will save you a ton over time, especially with today's prices.

- Insurance: This can vary wildly depending on the car’s make, model, age, and even its safety features. A zippy sports car will almost always cost more to insure than a sensible sedan.

- Maintenance and Repairs: Ah, the dreaded repair bill. Some cars are known for being more reliable and cheaper to fix than others. Do a little digging into the long-term reliability and typical maintenance costs for the models you're considering. A brand-new luxury car might have a lower initial sticker price than you think, but those specialized parts and labor can add up faster than you can say "uh-oh."

- Taxes and Fees: Don't forget registration fees, annual taxes, and any other government-imposed costs. These vary by location, so do your homework.

So, when you’re looking at two cars, one for $20,000 and another for $22,000, the $22,000 one might actually be cheaper in the long run if it has better fuel economy and lower maintenance costs. It’s about the total picture, not just the initial splash of paint.

The "Can I Actually Afford This?" Reality Check

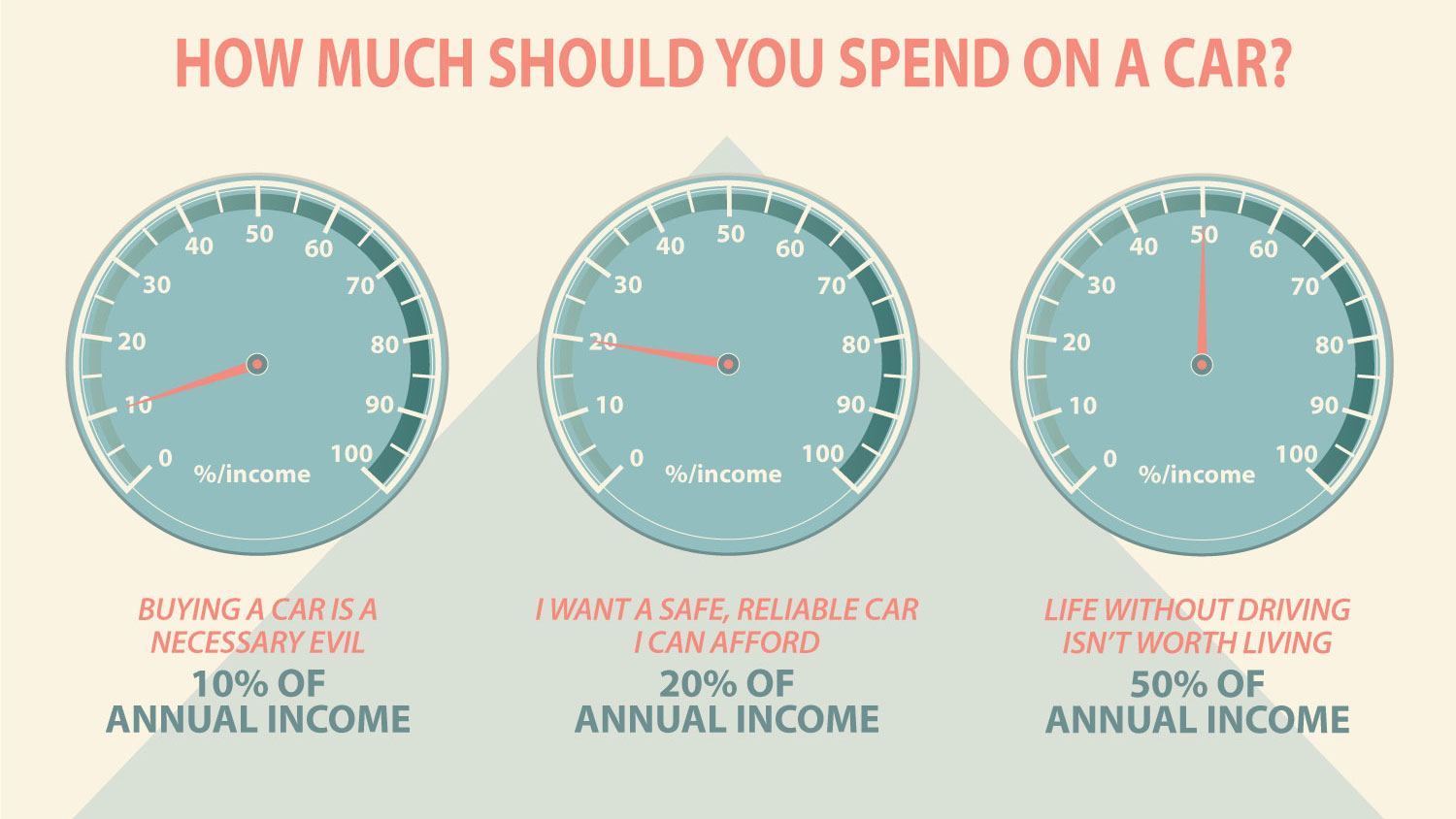

Now, let’s talk about the money part. This is where we get down to brass tacks, or in this case, dollars and cents. The golden rule? Don't stretch yourself too thin. Think of your car budget like your grocery budget. You can’t just decide to buy steak every night if your income only supports pasta. Your car payment should fit comfortably within your monthly expenses, not take over your life.

A good rule of thumb, and this is just a guideline, is the 20/4/10 rule. It's not a strict law, but a helpful nudge:

- 20% Down Payment: Aim to put down at least 20% of the car's price. This reduces your loan amount and can help you avoid negative equity (owing more on the car than it’s worth).

- 4-Year Loan Term: Try to finance the car over no more than four years. Longer loan terms mean lower monthly payments, but you’ll pay more interest overall, and the car will likely be worth less than what you owe for a significant portion of the loan.

- 10% of Gross Monthly Income: Your total car expenses – loan payment, insurance, and fuel – should not exceed 10% of your gross monthly income. This is a big one. It ensures you have plenty of room for rent/mortgage, food, utilities, and, you know, fun stuff!

Let's say your gross monthly income is $5,000. That 10% means your total car expenses should ideally be around $500 per month. If insurance and fuel are $200, that leaves you with $300 for a car payment. This might not get you that brand-new luxury SUV, but it could get you a perfectly good, reliable sedan or a slightly older, well-maintained SUV. And that’s perfectly okay!

It's also super important to consider what you can realistically afford for a monthly payment. Some people are great at making big down payments, others prefer smaller monthly payments. Work with your bank or credit union to get pre-approved for a loan before you even go to the dealership. This gives you a clear budget and a lot more negotiating power.

New vs. Used: The Eternal Debate

Ah, the age-old question! New cars smell amazing, have that fresh-off-the-assembly-line gleam, and come with all the latest gadgets. But they also come with the steepest depreciation. That brand-new car loses a significant chunk of its value the moment you drive it off the lot. It's like buying a brand-new, designer outfit and then immediately spilling coffee on it – a little heartbreaking!

Used cars, on the other hand, have already taken that initial depreciation hit. You can often get a lot more car for your money in the pre-owned market. Think of it like buying a gently used designer handbag. It’s still high-quality and stylish, but at a fraction of the original cost.

The key with used cars is to do your homework. Get a pre-purchase inspection from a trusted mechanic. Look for certified pre-owned vehicles, which often come with extended warranties. And don't be afraid of a car that's a few years old, especially if it has a good maintenance record. A 3-year-old car that's been well cared for can be a fantastic value.

If you're looking at a $30,000 new car, you might be able to get a comparable, well-maintained used car from a few years ago for $20,000 or even less. That’s a huge saving! Or, you could buy a $20,000 used car and have a significantly lower monthly payment, freeing up money for other life goals.

Don't Be Afraid to Walk Away

This is perhaps the most powerful advice I can give you. Dealerships are businesses, and they want to make sales. They're skilled at making you feel like this is the only car that will ever make you happy, or that this is the best deal you'll ever get. Remember that coffee-stained designer outfit analogy? Don't let yourself get caught up in the moment.

If a deal feels off, if the numbers don't add up, or if you feel pressured, it is perfectly okay to walk away. There are countless other cars out there. The pressure to buy is a common sales tactic. Take a deep breath, thank them for their time, and go home to think it over. You might be surprised to get a call back with a better offer!

So, how much should you spend on a car? There’s no single magic number. It’s a personal journey. It’s about understanding your life, being realistic about your finances, and doing your research. It’s about finding that sweet spot where your transportation needs are met without sacrificing your peace of mind or your ability to enjoy life’s other wonderful things. Happy car hunting!