How Much Is A Widow's Pension Uk

So, you're wondering about a widow's pension in the UK? It’s a bit like a treasure hunt, isn't it? Not a buried chest of gold, exactly. But definitely something people are curious about. And let's be honest, talking about pensions can be as exciting as watching paint dry. But this? This has a bit more… oomph.

Think of it this way: it’s not just about money. It’s about a bit of peace of mind. A little safety net. Especially when life throws you a curveball.

The Big Question: How Much Are We Talking?

Right, let's get to it. The million-dollar question, or perhaps the £100-a-week question. It’s not a fixed amount, you see. It’s a bit of a chameleon. It changes depending on a few things. Like a recipe, you need the right ingredients.

Must Read

One of the main ingredients? It’s all about the deceased partner. Were they paying National Insurance? For how long? This is pretty key.

If your dearly departed loved one paid enough National Insurance contributions, they might have qualified for a state pension. And guess what? You, as their widow (or widower, let’s not forget them!), might be able to claim a pension based on their contributions.

It’s Not Just About Love, It’s About NI!

It sounds a bit unromantic, doesn’t it? "Oh darling, did you pay enough National Insurance?" But it’s the reality of the system. Think of it as a posthumous thank you for all their hard work and tax-paying years.

There are two main types of state pension that might come into play. The first is the Widowed Parent's Allowance. This one is for when you have children. It helps with the bills when you're a single parent. And let’s face it, that’s a big job!

Then there's the Widow's Pension itself, which is now officially called Bereavement Support Payment. See? Even the names change! It’s like a secret code. But we’re cracking it, aren’t we?

Bereavement Support Payment: The Modern Take

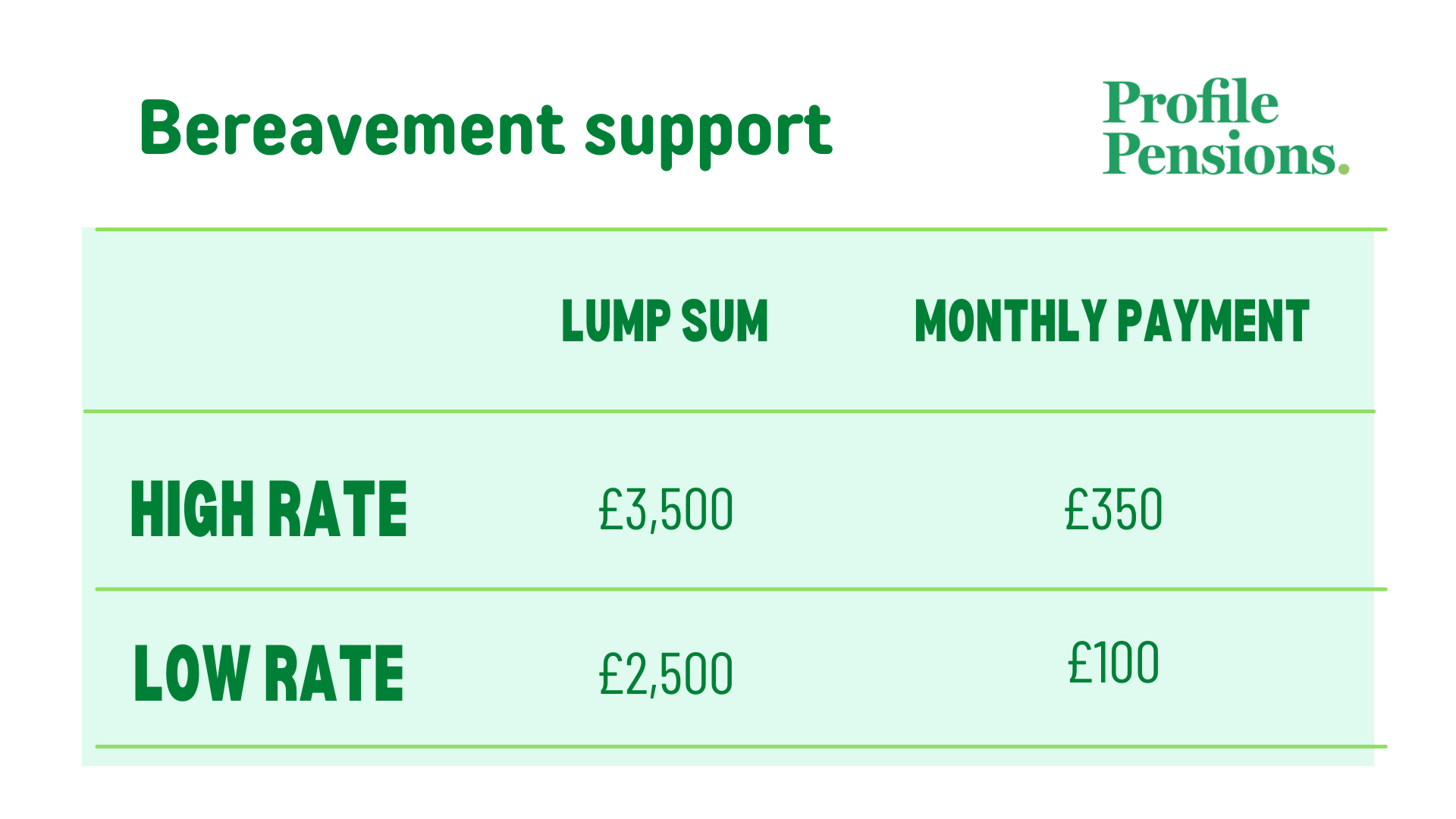

This is the current system. It replaced the old Widow's Pension. And it’s designed to give you a bit of breathing room. For up to 18 months.

There are two rates. A standard rate and a higher rate. The higher rate is for those with children. Because, as we know, kids cost an arm and a leg. And a childhood.

The standard rate gives you a lump sum first. Then a monthly payment for 18 months. The higher rate gives you a bigger lump sum. And then a bigger monthly payment. For those 18 months.

But here’s a quirky fact: the lump sum isn’t always paid straight away. Sometimes it can take a bit of time. So, it’s not always instant cash. Patience, my friend, is a virtue. Especially with government payments!

What About the Old System? The "Grandfathered" Pensions

Now, here’s where it gets a bit more complicated. And, dare I say, a little bit fun to unravel. If your partner died before a certain date (April 6, 2016, to be precise), you might be on the old Widow's Pension system.

This old system is different. It’s a weekly payment. And it can continue for as long as you’re a widow. No 18-month limit here!

But! And there’s always a "but," isn’t there? The amount you get is linked to your late partner’s National Insurance contributions and their age when they died.

It can also be affected by your own earnings. If you start working and earning more than a certain amount, your pension might be reduced. It’s like a balancing act. Earn too much, and the pension shrinks. Earn too little, and you might not be comfortable.

The Nitty-Gritty: How to Find Out for Sure

So, how do you actually find out what you’re entitled to? You can’t just guess. And you definitely can’t ask your neighbour’s cat. Although, wouldn’t that be a story!

The main place to go is Gov.uk. It’s the official government website. Think of it as the treasure map. You need to follow the clues.

You can also call the Bereavement Service. They are the keepers of the secrets. They can tell you if you're eligible and how much you might receive. Don’t be shy. They’re there to help.

Gather your information. Your partner’s National Insurance number. Their date of birth. Their death certificate, of course. These are your golden tickets.

Is It Worth Claiming? The Big Decision!

This is where the fun really starts. Is it worth navigating the system? Is it worth the paperwork?

For most people, the answer is a resounding yes!

Even a small amount can make a difference. Especially when you’re dealing with grief. The last thing you want is to worry about bills.

And remember, the old Widow’s Pension could be for life. That’s a pretty significant benefit. It’s not just pocket money. It’s a regular income stream.

Quirky Facts and Funny Bits

Did you know that the rules for pensions have changed quite a bit over the years? It’s like a historical drama. Different acts, different rules.

The Bereavement Support Payment is designed to be simpler. But sometimes, simpler can still be… a puzzle.

And let’s talk about the names. "Widow's Pension." It sounds so… classic. Like something from a black and white film. Then you have "Bereavement Support Payment." Very modern. Very… practical.

Imagine a widow from the 1950s. She’d probably be a bit baffled by the current system. And we, in turn, might find some of the old rules utterly bizarre.

The "Partner" Definition: A Little Twist

One little quirky thing to consider is who counts as a "partner." Usually, it’s a spouse or a civil partner. But there are some exceptions. If you were living together as if you were married for a certain period, you might still be eligible.

It’s not always as straightforward as a wedding certificate. It’s about the reality of your relationship. A bit of a romantic loophole, perhaps?

But don’t go getting too excited about loopholes. The criteria are quite strict. You still need to prove the nature of your relationship.

The Bottom Line: It's About Support

Ultimately, a widow's pension in the UK is about providing support. It’s about acknowledging the loss and offering a helping hand. Whether it’s the old system or the new, it’s there to help.

It’s not a lottery win. It’s not a guaranteed fortune. But it is a vital part of the social safety net.

So, while the exact amount can be a bit of a mystery, the intention behind it is clear. To help people through a difficult time. And that, my friends, is definitely something worth talking about. Even if it involves a few more forms than we’d like.

Don’t be afraid to ask questions. Don’t be afraid to dig for the answers. Your future financial well-being might just depend on it. And who knows, you might even find it a little bit interesting. Dare I say, even… fun?