Does A Sole Trader Have Unlimited Liability

Ever dreamt of ditching the corporate grind and becoming your own boss? Maybe you’re a whiz with sourdough, a maestro of macramé, or you’ve got a knack for fixing leaky taps that makes plumbers weep with envy. Whatever your passion, the idea of being a sole trader sounds pretty sweet, right? No boss breathing down your neck, calling the shots, and all the profits (well, mostly!) landing in your own pocket. It’s like being the captain of your own ship, sailing the entrepreneurial seas.

But hold your horses, aspiring business moguls! Before you start printing those fancy business cards that say "Supreme Commander of [Your Awesome Business Name]," there's a little something called liability that you really, really need to get your head around. And for sole traders, it’s not just a little splash; it’s more like diving headfirst into the deep end, without a life vest. Yep, we’re talking about unlimited liability.

Now, “unlimited liability” sounds a bit like a Michelin-starred buffet – endless choices, endless delights! But in the business world, it’s more like an endless bill. Imagine this: you’re running a little side hustle selling your grandmother’s award-winning jam. It’s flying off the shelves, and then, disaster strikes. Someone takes a spoonful, has a severe allergic reaction (despite your meticulously labelled ingredients, of course!), and decides to sue. Or perhaps your best customer’s priceless antique vase gets accidentally knocked over during a delivery. Things happen, right? Life isn't always sunshine and perfectly preserved berries.

Must Read

When you’re a sole trader, your business and your personal life are basically intertwined. They’re not separate entities, like a perfectly folded sock in a drawer and a rogue sock that’s somehow ended up under the sofa. No, they’re more like two enthusiastic toddlers who’ve decided to paint the living room wall together. Messy, unpredictable, and hard to separate. So, if your jam business racks up some hefty debts, or if that lawsuit from the allergic jam connoisseur goes south, it’s not just the business’s bank account that’s in trouble. Oh no. It’s your bank account, your savings, your… well, pretty much anything you own.

Think of it this way: you’ve got a lemonade stand. Super cute, lots of fun. But if one day, little Timmy trips over your lemonade stand and breaks his arm, and his parents decide to sue for medical bills and emotional distress (because, you know, no lemonade for the rest of the day), they’re not just coming after your lemonade profits. They could, in theory, come after your piggy bank, your bike, even that beloved teddy bear you’ve had since you were tiny. It’s like the universe saying, "Surprise! That business risk you thought was contained? Nope, it’s all yours!"

The Nitty-Gritty of Being a Sole Trader

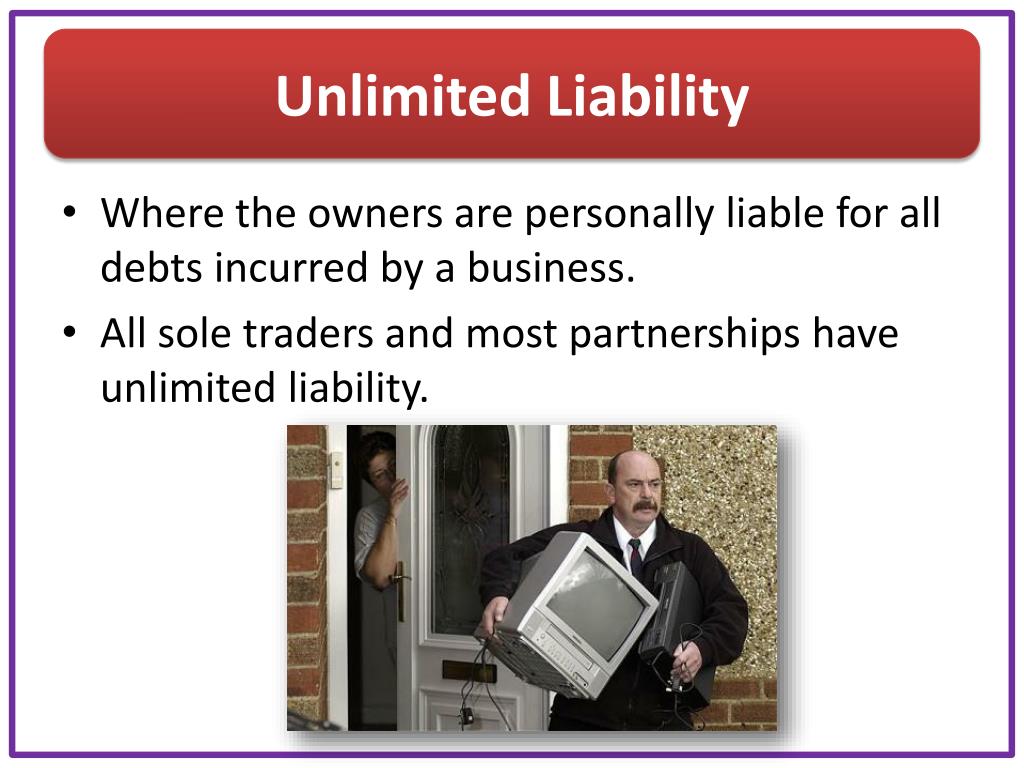

So, what does this “unlimited liability” actually mean in practical terms? It means that if your business owes money – be it to suppliers, the taxman, or someone you’ve wronged (accidentally or otherwise) – and the business can’t pay, then you, personally, are on the hook. This isn't just about the money you’ve invested in the business. This can extend to your personal assets. We’re talking about your house, your car, your savings, and even potentially your future earnings. It’s like a credit card with no limit, but instead of buying more gadgets, you’re liable for business debts.

Imagine you’ve started a small catering business. You’ve bought a fancy industrial-sized mixer, catering vans, and a mountain of napkins. Business is booming! Then, a global pandemic hits (you know, those little surprises that pop up every now and then!). Suddenly, all your events are cancelled. You still have bills to pay, loans to service, and staff (if you have any) to think about. If you can’t make ends meet, and the business folds, those debts don’t just vanish into thin air. They follow you home. The bank might come knocking on your door, not just for the business loan, but potentially for the value of your house if that’s what it takes to settle the debt.

It’s a bit like being a knight in shining armour, but instead of fighting dragons, you’re fighting off creditors with your own personal savings. You’re the ultimate guarantor, the final safety net. And sometimes, that net feels more like a tightrope over a very deep canyon. It’s a heavy responsibility, and it’s why many people, once their business starts to grow, opt to become a limited company. More on that later!

So, is it All Doom and Gloom?

Now, before you start packing away your dreams of being a freelance dog groomer or a bespoke furniture maker, let’s not get too carried away with the doom and gloom. Being a sole trader is incredibly popular for a reason. For many, especially when starting out, it’s the simplest and most cost-effective way to get your business off the ground. The paperwork is usually minimal, and the setup costs are far lower than for other business structures.

Think of it like this: starting as a sole trader is like borrowing your friend’s slightly-too-small bicycle for a quick spin around the park. It’s easy to get on, fun to ride, and you can usually get back to where you started without too much fuss. You don’t need to fill out a thousand forms to use it, and if you scuff it up a bit, it’s usually not the end of the world. It’s about agility and simplicity.

For small businesses, hobbyists who want to earn a bit of extra cash, or freelancers just dipping their toes into the water, being a sole trader is often the perfect fit. You can test your business idea, build up a customer base, and see if it’s something you want to pursue long-term, all with a relatively low barrier to entry. It’s a fantastic way to gain experience and build confidence.

The key is to understand the risks and to manage them as best you can. It’s like being a chef: you know that some ingredients can cause allergies, so you label everything carefully and are prepared to handle reactions. You don’t stop cooking; you just cook smarter and safer. And for many, that’s exactly what being a sole trader is all about.

Managing the Risk: The Sole Trader's Survival Guide

So, how do you navigate this whole “unlimited liability” minefield without ending up living in a cardboard box because your artisanal pickle business went belly up? It’s all about smart strategies and being prepared. It’s like playing a game of Jenga; you’re pulling out pieces, but you’re trying to be incredibly careful not to topple the whole tower.

Firstly, get insured. This is your knight in shining armour, your superhero cape, your… well, your really good insurance policy. Public liability insurance is your best friend here. If someone gets injured or their property is damaged because of your business, insurance can cover the costs. It’s like having a shield that deflects the most damaging blows. Professional indemnity insurance is also crucial if you offer advice or services that could lead to financial loss for your clients.

Secondly, keep your business and personal finances separate. I know, I know, it’s tempting to just dip into the business account for that last-minute birthday present, but resist! Open a dedicated business bank account. This makes it so much easier to track your income and expenses, and crucially, it helps to create a clearer line between your personal assets and your business’s obligations. It’s like having two different wardrobes: one for work and one for chilling at home. They shouldn’t be mixed up!

Thirdly, be incredibly diligent with contracts and agreements. If you’re providing a service or selling a product, have clear terms and conditions. This can help to manage expectations and protect you if something goes wrong. It’s like having a very detailed instruction manual for your business interactions. No one likes wading through legal jargon, but a well-drafted contract is like a secret handshake that keeps everyone on the same page and out of trouble.

Fourthly, don’t over-extend yourself financially. It’s tempting to buy all the shiny new equipment and stock up on every possible ingredient when business is good. But remember that the good times might not last forever. Try to keep your debts manageable and build up a healthy cash reserve for unexpected bumps in the road. It’s like packing a sensible lunch for a hike, not just a giant bag of sweets. You need sustenance for the long haul!

And finally, seek professional advice. Talk to an accountant or a business advisor. They can help you understand your obligations, plan your finances, and even advise you on when it might be the right time to consider a different business structure, like a limited company, if your business is growing and the risks are increasing.

When to Think About Going Limited

As your business grows, the potential for things to go wrong also grows. If your business starts to take off, you’re employing people, dealing with larger clients, or operating in a higher-risk industry, that’s when the idea of limited liability starts to sound really appealing. A limited company is a separate legal entity from its owners.

This means that if the company incurs debts or faces lawsuits, the liability of the owners (the shareholders) is generally limited to the amount they have invested in the company. So, if your limited company goes bust, you won’t typically lose your house or your personal savings. Your risk is usually capped at the value of your shares. It’s like having a superhero suit that protects your civilian identity. Your personal life is safe, even if your business cape gets a little torn.

Moving from a sole trader to a limited company involves more paperwork, more administration, and often, more costs. You’ll have to file annual accounts with Companies House, hold board meetings (even if it’s just you!), and generally comply with more regulations. It’s a bigger commitment, like graduating from that friend’s bicycle to buying your own professional racing bike – more complex, but built for speed and resilience.

However, for many growing businesses, the peace of mind that comes with limited liability is well worth the extra effort. It allows you to take on bigger projects, attract investment, and generally operate with a greater sense of security. It’s about scaling up your protection as you scale up your ambitions.

So, does a sole trader have unlimited liability? In short, yes, they absolutely do. It’s a fundamental aspect of being a sole trader, and it’s the price of that initial simplicity and freedom. It’s not a reason to abandon your entrepreneurial dreams, but it is a very good reason to be informed, to be cautious, and to be prepared. Think of it as the ultimate entrepreneur’s lesson in risk management. Master it, and you can focus on what you do best: building an amazing business!