Difference Between Finance Lease And Operating Lease

Alright, let's talk about leases. Now, I know what you're thinking: "Leases? Isn't that just for fancy businesses with their fleets of limousines and humongous office buildings?" Well, sort of, but the ideas behind leases pop up in our everyday lives way more than you'd think. It's like trying to figure out if you're buying that really cool gadget, or just borrowing it for a while with the option to keep it later. Today, we're going to untangle the difference between two main types of business leases: the finance lease and the operating lease. Think of it as the difference between getting a new puppy that's yours to train and love forever, versus pet-sitting your neighbor's adorable, but ultimately not-yours-to-keep, poodle for the summer.

Imagine you're eyeing that shiny new espresso machine for your home office. You really want that barista-level latte art. You've got a few ways to get it. You could plonk down all your cash right then and there. Or, you could take out a loan and pay it off over time. Or… you could lease it. And just like with the espresso machine, businesses have these leasing options for big-ticket items like machinery, vehicles, or even software. The core idea is getting to use something without owning it outright from day one.

So, what's the big deal with finance leases versus operating leases? It all boils down to who's treating the asset like they own it, and who's just enjoying its use for a bit. It’s like the difference between when your kid really wants that video game controller, versus when they're just borrowing your phone to watch cartoons.

Must Read

The Finance Lease: It's Practically Yours, Just Not Officially Yours (Yet!)

Let's dive into the finance lease first. Think of this one as the lease that really, really wants to be a purchase. It's like when you're renting a fancy apartment, but the lease is so long, and you've put in so many custom shelves and painted the walls your favorite color, that it feels like yours. You're making payments that are pretty substantial, and by the time the lease is up, you've basically paid off most of the value of the asset.

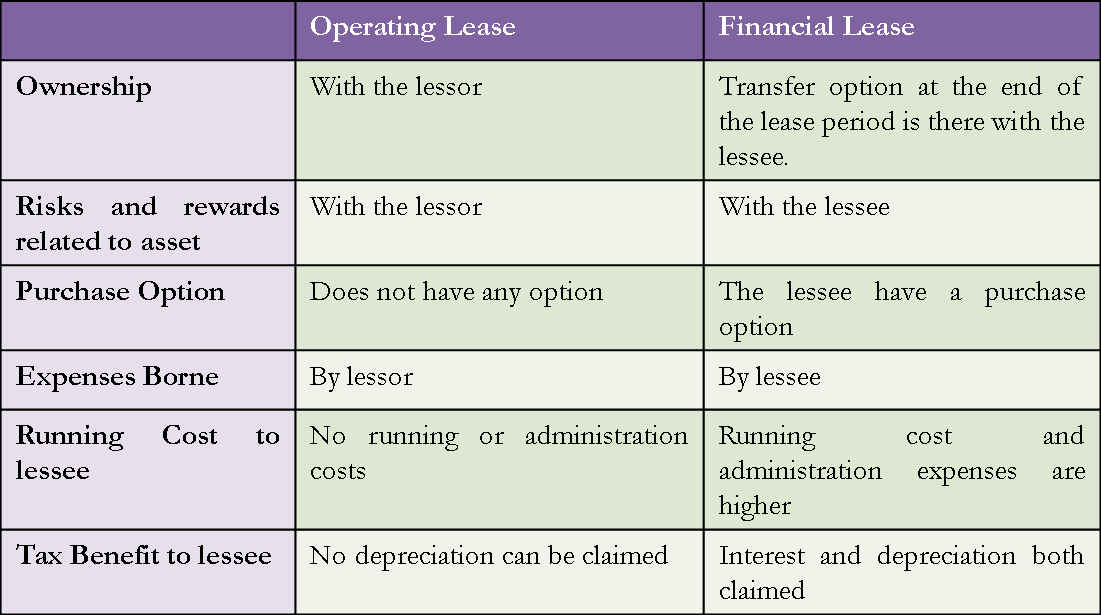

In finance lease land, the lessee (that's the person or company doing the leasing, not the owner) takes on most of the risks and rewards of owning the asset. It’s like you get the car with all the bells and whistles, you’re the one worrying about the oil changes, the tire rotations, and whether that mysterious rattle is going to turn into a full-blown engine disaster. The lessor (the owner) is kind of sitting back, collecting their payments, but they’re not as hands-on with the day-to-day stuff.

Here's a funny way to think about it: imagine you’re “leasing” your kid’s college education. You’re paying for it, you’re worried about their grades, you’re involved in their extracurriculars – it’s a huge commitment, and at the end, you’ve invested so much, it’s almost like you own the degree (or at least a significant chunk of it!).

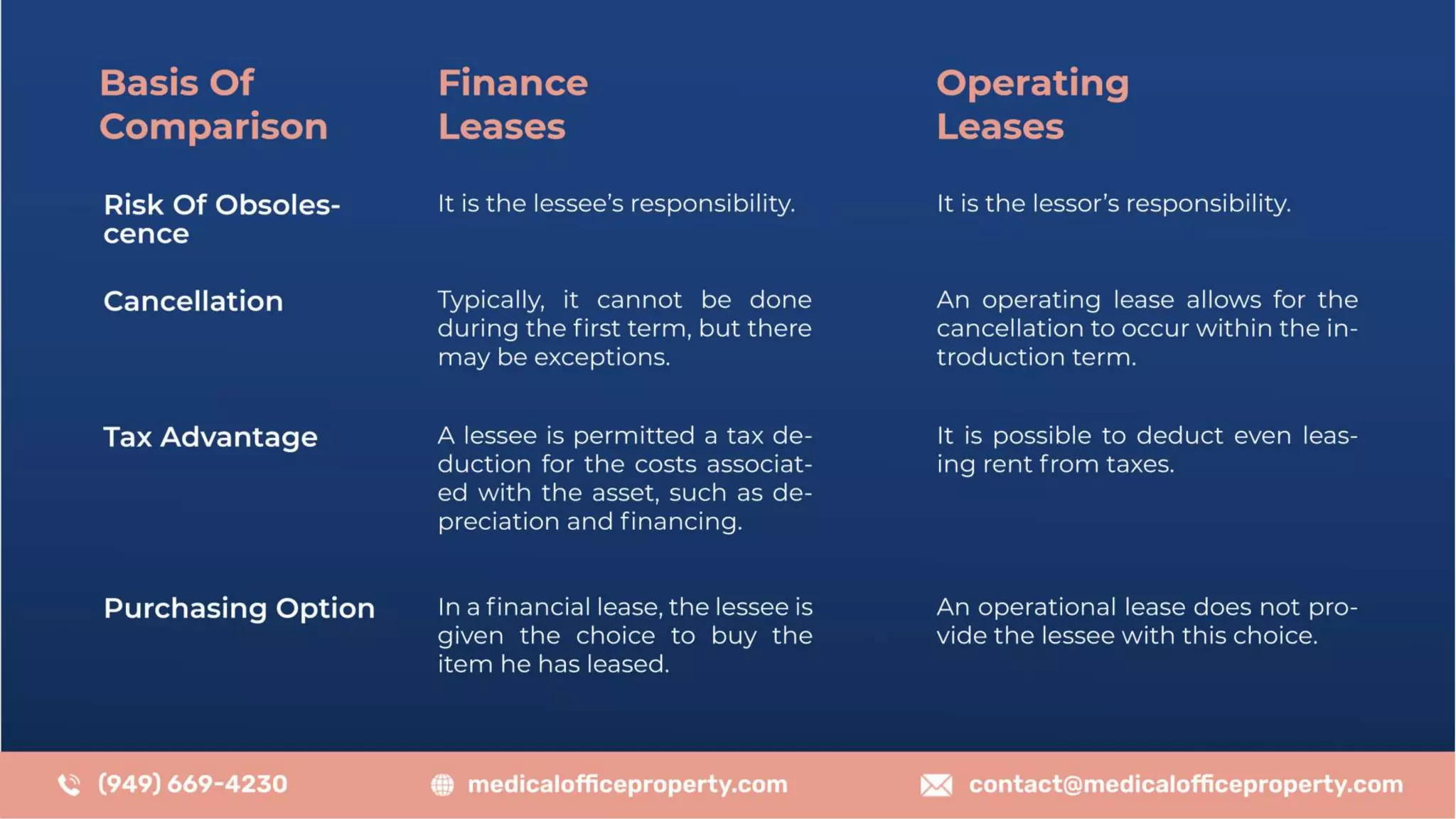

A key characteristic of a finance lease is that it typically covers a major part of the asset's economic life. Think of it as a long-term relationship, not a casual fling. You’re signing up for the long haul. And usually, there's an option to buy the asset at the end for a bargain price, or even a zero dollar purchase option. It’s like the rental car company saying, "You know what? After three years, just give us a dollar and it's yours. Deal?"

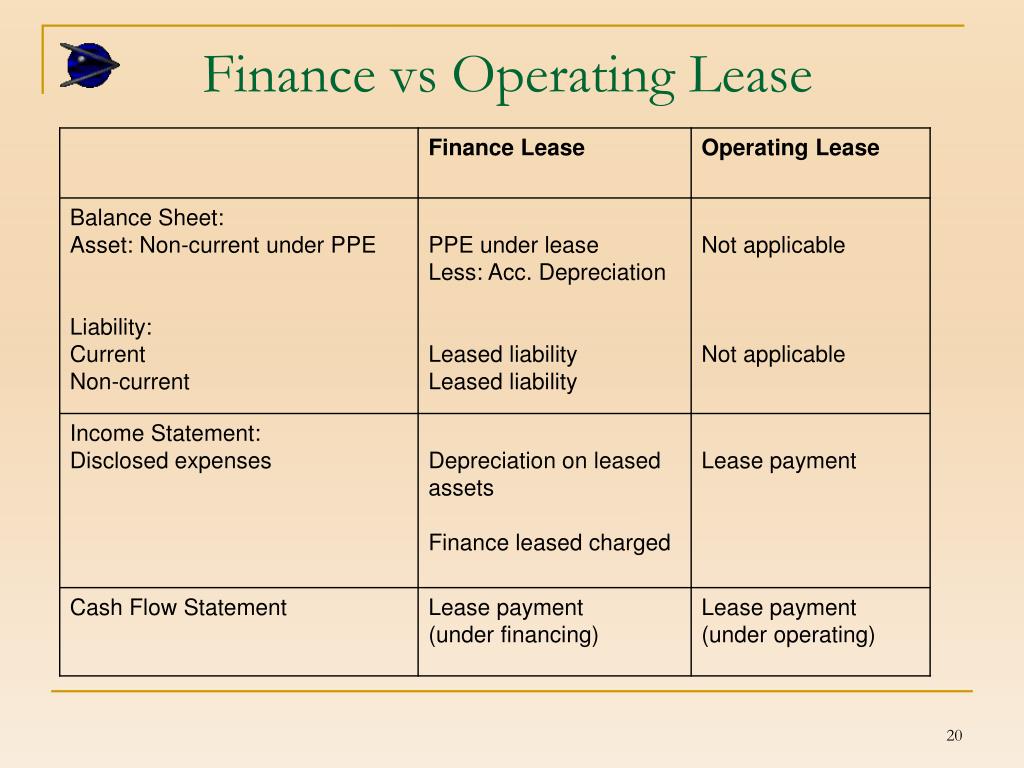

From an accounting perspective, a finance lease gets treated as if the lessee owns the asset. It appears on their balance sheet, and they depreciate it. This is because, from a substance-over-legal-form perspective, the economic reality is that the lessee has effectively acquired the asset. It's like if your friend "borrows" your favorite jacket for so long, and uses it so much, and you know they’ll never give it back, you start mentally writing it off as theirs anyway.

The payments for a finance lease are also calculated to cover the full cost of the asset, plus interest. So, you're essentially paying for the asset and a little extra for the privilege of using it over time. It’s like taking out a loan to buy that espresso machine – you pay back the machine's cost plus the interest. It’s a financial commitment, a big one.

Think of it this way: You're not just renting a tool; you're entering into an agreement that looks and feels a lot like buying it, just with a slightly more complicated payment structure.

The Operating Lease: Renting for the Fun of It (Mostly)

Now, let’s switch gears and talk about the operating lease. This is the lease that feels more like… well, a rental. It's more flexible, usually shorter-term, and the lessor retains most of the risks and rewards of ownership. It’s like renting a tuxedo for a wedding. You get to look sharp, but you’re not worried about the dry cleaning bills for the next decade, and you definitely don’t plan on wearing it to Thanksgiving dinner next year.

With an operating lease, the lessee is simply using the asset for a period of time, and at the end, they hand it back to the lessor. It’s like you’re renting a car for your vacation. You enjoy the ride, you keep it clean (hopefully!), but when you return it to the airport, your responsibility is pretty much over. You don't worry about its resale value or whether it needs new tires.

The payments for an operating lease are generally lower than for a finance lease. Why? Because you're not paying to own the asset; you're paying for the use of it. It’s like paying a monthly subscription for a streaming service. You get to watch all the shows, but you don’t own the movie studio or the rights to the films.

A really common example of an operating lease in real life is your office printer. You probably don’t own that behemoth. You lease it, get a certain number of copies per month, and when the contract is up, the leasing company takes it away and gives you a new one. They’re the ones responsible for maintenance, repairs, and figuring out what to do with the old printer. You just worry about making sure you don't run out of toner during that crucial presentation.

The lease term for an operating lease is typically much shorter than the asset's economic life. Think of it as a seasonal rental, or a short-term fling. You use it, enjoy it, and then move on. There's usually no option to buy the asset at the end, or if there is, it's at fair market value, which means you're not getting any special deal.

From an accounting standpoint, operating leases are treated as off-balance sheet items (though accounting rules have evolved, so this can be more nuanced now!). This means they don't show up as an asset or a liability on the lessee's balance sheet. The lease payments are simply expensed as they occur. It's like when you pay for your gym membership – you use the gym, you pay the fee, but the gym equipment isn't listed on your personal balance sheet.

Think of it this way: You're renting a service, a temporary solution, without the long-term commitment or the financial burden of ownership.

So, What's the "Real" Difference? Let's Break It Down Like a Pro (Who Loves Snacks)

Okay, let’s boil it down with some everyday analogies. Imagine you’re getting a dog.

Finance Lease is like adopting a puppy.

- You're committed: You're signing up for years of wagging tails, early morning walks, and vet bills.

- It feels like yours: You're naming it, training it, and buying all the chew toys.

- You're responsible: You're cleaning up the messes, making sure it’s fed, and generally dealing with all the ups and downs of dog ownership.

- At the end (of its life, perhaps), you've invested so much time and money, it’s like you’ve “owned” that furry friend. There's no "returning" the dog.

Operating Lease is like pet-sitting your friend's adorable, but slightly mischievous, dog for the summer.

- Temporary gig: You know Fido is going back to his real home after Labor Day.

- Enjoy the fun: You get to play fetch, go for walks, and enjoy the company.

- Responsibility is limited: Your friend is still providing the main food, the vet visits are their problem, and you're not dealing with house-training regressions.

- Hand-off: When summer ends, you hand Fido back, and you’re free to go on vacation without worrying about dog sitters.

Another comparison: Let’s talk about your phone.

Finance Lease: You get the latest iPhone, sign a 2-year contract, and pay a monthly fee that’s basically financing the phone. By the end of the contract, you’ve paid off most of its value, and you have the option to buy it for a small amount, or trade it in for a new one (which is like a new lease!). You're bearing the risk of it falling out of your pocket and shattering – you’re responsible for its upkeep.

Operating Lease: You sign up for a phone plan where you can swap out your phone every year or two. You pay a monthly fee, use the phone, and then return it to get the newest model. The phone company owns the phone; you're just paying for the service and the use of the latest tech. They worry about the resale value and what happens to the old phones.

Why Does This Matter for Businesses?

For businesses, the distinction between these two types of leases has significant implications for:

- Accounting: As we touched on, how it appears on the balance sheet affects financial ratios and how investors see the company.

- Taxation: There can be different tax treatments for lease payments depending on the type of lease.

- Cash Flow: Operating leases often involve lower upfront payments and smoother cash outflow, which can be attractive for companies wanting to conserve cash. Finance leases, on the other hand, can feel more like a capital investment.

- Flexibility: Operating leases generally offer more flexibility to upgrade or change assets as technology or business needs evolve.

Imagine a startup that needs a whole fleet of delivery vans. They might opt for operating leases on the vans. This allows them to get the vehicles they need to operate without a massive upfront capital expenditure. As their business grows and their needs change, they can more easily adjust the number of vans or upgrade to newer models. If they were to finance-purchase all those vans, it would tie up a huge amount of their limited capital.

On the flip side, a well-established manufacturing company that needs a highly specialized piece of machinery for a specific, long-term project might opt for a finance lease. They know they'll need this exact machine for the next 10 years, and it makes sense from an accounting and financial perspective to essentially "buy" it over time, taking on the full benefits and risks of ownership.

The Bottom Line: It's All About Ownership (or Lack Thereof!)

Ultimately, the difference between a finance lease and an operating lease comes down to who is bearing the majority of the risks and rewards of ownership. It’s about whether the lease agreement is structured to transfer the economic substance of ownership to the lessee (finance lease), or if it’s primarily a rental agreement for the use of an asset (operating lease).

So, next time you hear someone talking about leases, you can casually nod and say, "Ah yes, the finance lease versus the operating lease. It's like the difference between buying your dream home with a mortgage versus renting a beachfront bungalow for the summer." And then, perhaps, you can both chuckle and agree that leases, like good snacks, are sometimes necessary for getting by.