Difference Between A Standing Order And Direct Debit

Ever feel like your bank account is playing a game of hide-and-seek with your bills? You know money needs to go out, but keeping track of when and how much can be a mini-adventure in itself. That’s where our trusty payment pals, Standing Orders and Direct Debits, come in! Think of them as your personal financial ninjas, silently ensuring your regular payments are sorted without you having to lift a finger (or remember a date!). Learning the difference isn’t just about being financially savvy; it’s about unlocking a smoother, less stressful way to manage your money. It’s like having a secret code to unlock peace of mind, and who doesn’t want that?

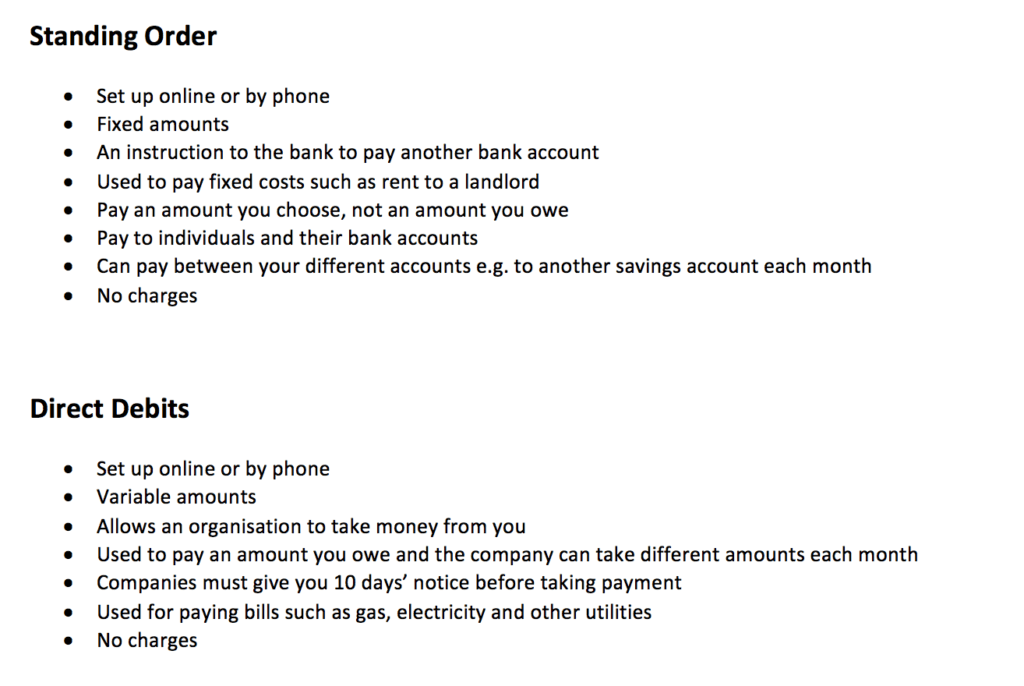

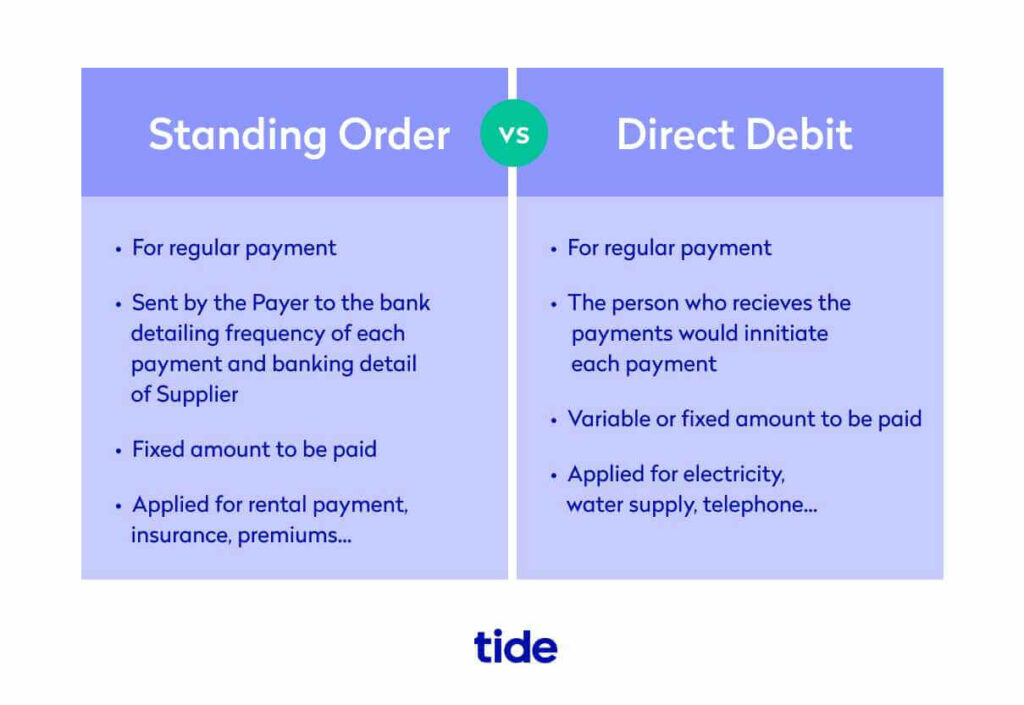

The Humble Standing Order: Your Reliable Reminder

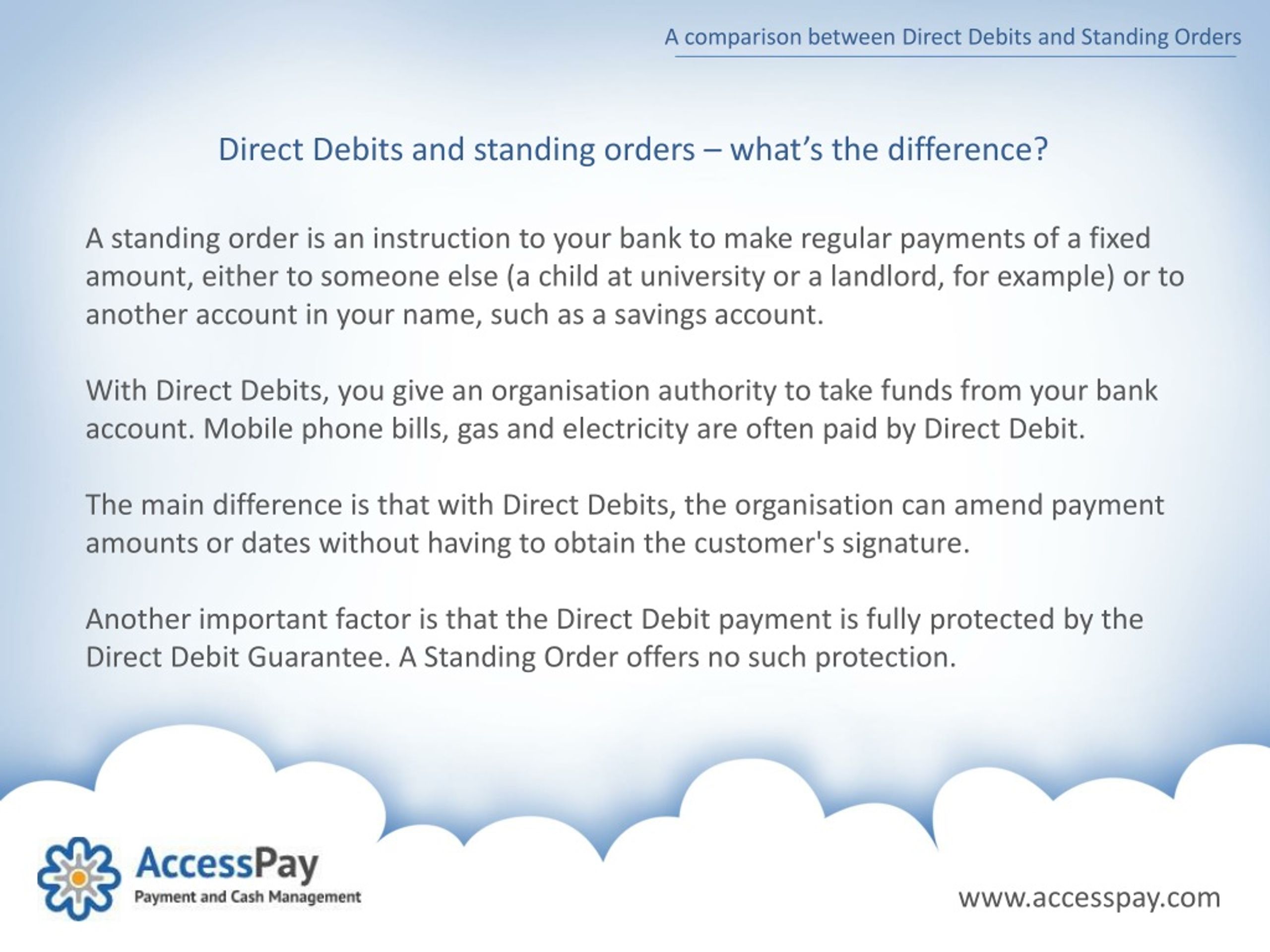

Imagine you have a subscription to your favourite magazine, a regular payment to a friend who’s helping you out, or you’re consistently saving a portion of your salary into a separate account. For these kinds of payments, where the amount and the date are pretty much fixed, a Standing Order is your go-to hero. It’s essentially an instruction you give to your bank to pay a specific amount of money to another bank account on a regular basis. You decide the amount, you decide the frequency (weekly, monthly, yearly – you name it!), and you decide the start and end date.

The beauty of a Standing Order lies in its predictability. Since you set the rules, the amount and date will stay the same unless you tell your bank otherwise. This makes it perfect for things like:

Must Read

- Regular Savings: Building up that holiday fund or rainy-day stash has never been easier. Set it and forget it!

- Rent or Mortgage Payments: If your rent or mortgage is always the same amount, a standing order ensures it’s paid on time, every time.

- Payments to Family or Friends: Helping out a family member or paying back a mate regularly becomes effortless.

- Fixed Subscriptions: For services with a consistent monthly fee, like certain gym memberships or online courses.

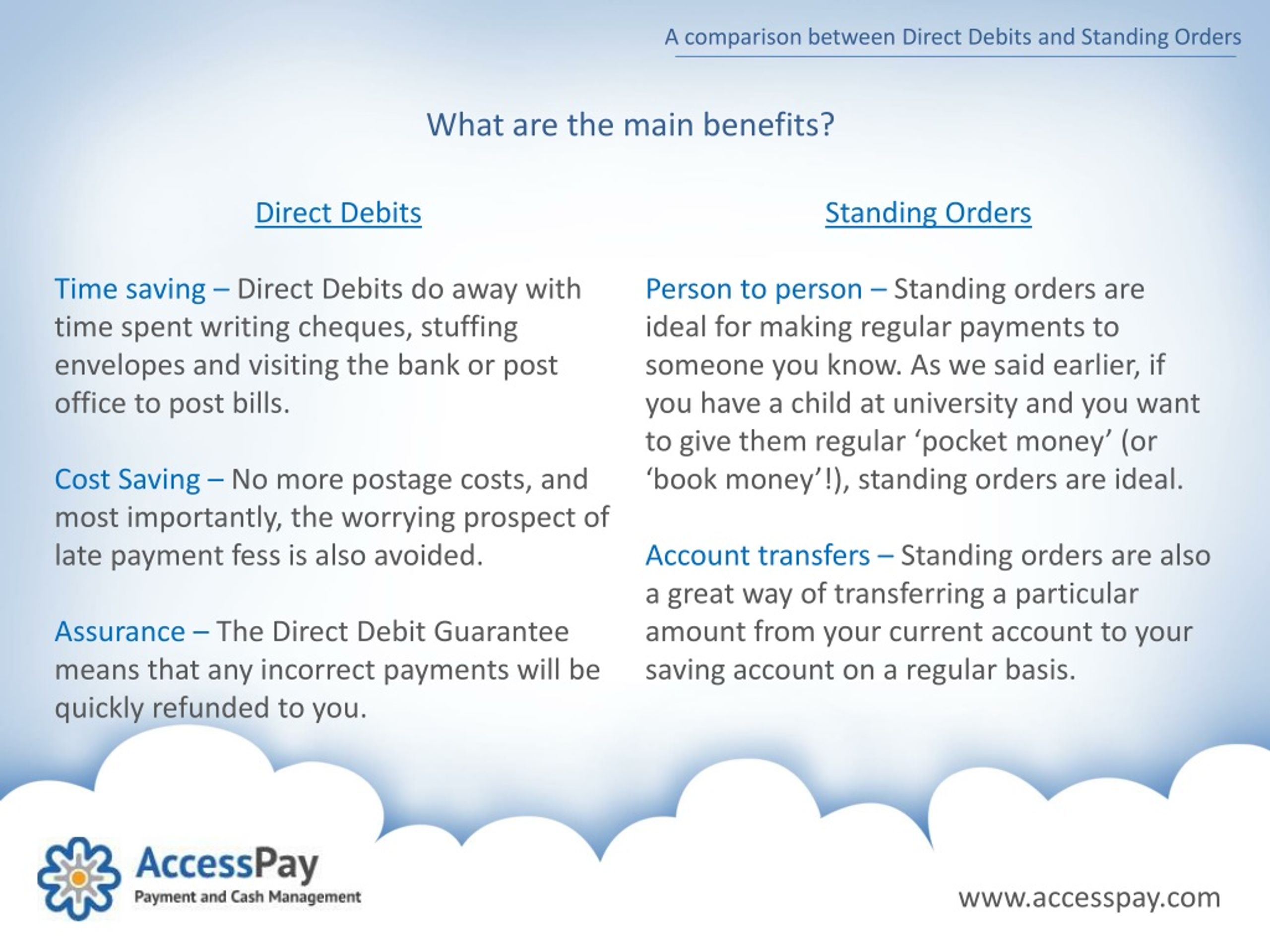

The benefits are crystal clear: control and simplicity. You know exactly how much is leaving your account and when. It’s a straightforward way to manage fixed outgoing payments, giving you a solid grip on your budget.

Enter the Mighty Direct Debit: The Flexible Friend

Now, let’s talk about Direct Debit. This is a bit of a different beast, and it’s fantastic for those payments where the amount might change, or where you’re authorising a company to take money from your account.

With a Direct Debit, you give permission to a company or organisation (the "biller") to take payments directly from your bank account. Crucially, they control the amount and the date of the payment, based on the agreement you have with them. But don’t worry, it’s not a free-for-all! You’ll always receive a notification from the biller in advance, telling you how much they’ll be taking and when. This gives you a heads-up to ensure you have sufficient funds in your account.

Direct Debits are incredibly common for:

- Utility Bills: Gas, electricity, water – these often fluctuate, so a Direct Debit handles the variable amounts.

- Phone and Internet Contracts: Your monthly mobile or broadband bill can change based on usage or new deals.

- Credit Card and Loan Repayments: These amounts can vary, especially with interest.

- Subscriptions with Variable Fees: Think of streaming services that might have different tiers or premium options.

The main benefit of a Direct Debit is its flexibility and convenience. It’s the perfect solution for bills that aren’t the same every month. Plus, they come with built-in protection. Under the Direct Debit Guarantee, if an error is made in the payment, you're entitled to an immediate refund from your bank. This is a fantastic safety net!

Standing Order vs. Direct Debit: The Showdown

So, what’s the key takeaway? It’s all about who’s in charge and whether the amount is fixed.

Standing Order:

- You set the amount and date.

- Best for fixed, regular payments.

- You initiate the instruction to your bank.

Direct Debit:

- The company you're paying sets the amount (with your prior agreement and notification) and date.

- Best for variable or fluctuating payments.

- You give permission to the company to collect funds.

- Comes with the Direct Debit Guarantee for protection.

Think of it this way: a Standing Order is like writing a cheque that automatically gets delivered on the same day every month for the same amount. A Direct Debit is more like giving someone a key to your letterbox, but they have to tell you what they're taking out beforehand and promise to give it back if they mess up. Understanding which one to use for different payments can save you time, hassle, and even protect you from overpaying or missing a bill. So, next time you’re setting up a new payment, just ask yourself: is the amount fixed? And who’s driving this money train? Your answer will tell you whether to call for your Standing Order friend or your Direct Debit companion!