Average Uk Pension Pot

Alright, settle in, grab your cuppa, because we're about to dive into a topic that's about as exciting as watching paint dry, but trust me, it's got some hidden comedy gold. We're talking about the average UK pension pot. Yes, that magical nest egg we're all (supposedly) building for our golden years. Now, before you imagine vast piles of cash, let's just say the reality might be a tad… less glamorous than a Bond villain's vault.

Imagine this: you're at a bustling café, the air thick with the scent of coffee and maybe a hint of existential dread about the future. Your mate leans in conspiratorially and asks, "So, how's that pension looking, eh?" You stammer something about "it's… growing?" and then the conversation takes a turn.

According to the latest intel, the average UK pension pot for someone nearing retirement is hovering around the £60,000 mark. Sixty. Thousand. Pounds. Now, if you're picturing a luxury cruise around the world, with champagne flutes clinking and personal butlers fawning over you, you might need to recalibrate your expectations. This amount, for many, is more like enough for a very comfortable weekend break… in Margate. With packed lunches.

Must Read

But hang on, before you start weeping into your latte, let's break it down. £60,000 sounds like a lot of pennies, right? It is! It's just that, when you're talking about funding potentially 20, 30, or even 40 years of not having to get up for work at 7 am, it starts to feel a bit like trying to fill a bathtub with an eyedropper. A very, very slow eyedropper.

And here’s a juicy bit of tea: this £60k isn't a homogenous blob of cash. Oh no. This figure is often heavily skewed by a few individuals with absolutely ginormous pension pots. Think of it like this: if Jeff Bezos joined your local pub quiz team, the average score would skyrocket, but it wouldn't necessarily reflect how well Brenda from Accounts knows her 80s power ballads. So, for many of us regular folk, our actual pension pot might be significantly smaller. Much smaller. Like, "hope the grandkids bring you biscuits" smaller.

The truth is, the average pension pot is a bit of a red herring. It's like looking at the average speed of a car on a motorway – it doesn't tell you if that car is a supercar doing 120mph or a little Fiat 500 stuck in traffic at 30mph. And let's be honest, most of us are probably in the Fiat 500 camp when it comes to our pensions.

So, where does this £60,000 figure come from? Well, it’s a combination of state pensions, private pensions, workplace pensions, and those slightly-embarrassing-but-necessary-when-you're-older SIPP accounts. Workplace pensions have made things so much better, with auto-enrolment meaning millions are now saving without even thinking about it. It’s like getting a surprise bonus, except the bonus is… future you’s money. Sneaky!

But even with auto-enrolment, the contributions can still be quite modest. And over the years, inflation, market fluctuations, and the sheer temptation to dip into that pot for a new telly can all take their toll. Ever seen a pension statement that looks like it's been through a blender? Yeah, me neither. But I've heard stories.

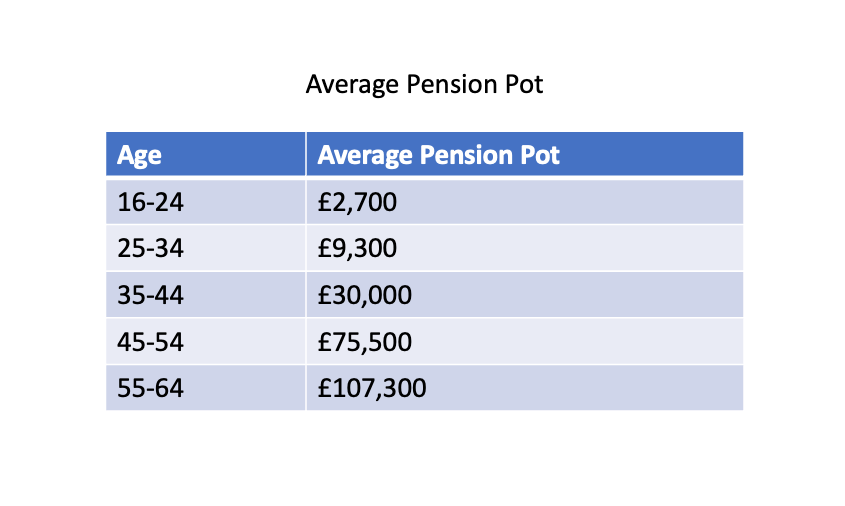

Let's add another layer of delightful confusion. The £60k figure is often for those approaching retirement. What about younger people? Well, for those in their 20s and 30s, the average pot is… well, let's just say it's a number that would make a squirrel blush. Some surveys show figures as low as a few thousand pounds. Which, again, is great for buying a fancy coffee machine, but not so much for a lifetime of leisure.

It’s a bit of a worrying trend, isn't it? We’re living longer, which is fantastic! More time to enjoy life, see the world, and perfect our sourdough starter. But living longer also means our savings need to stretch further. That £60,000 might need to last you longer than a discount airline flight on Christmas Eve.

Now, I’m not trying to be a doom-monger. Far from it! This is a story with potential for a happy ending. The key is understanding the situation. If your pension pot is currently more of a "pension puddle," don't panic. It's never too late to take action. Think of it as a surprise plot twist in your financial thriller.

First things first: check your statements. Yes, I know, it’s about as thrilling as watching grass grow, but it’s crucial. See where you’re at. Are you contributing enough? Are your investments performing reasonably well? If your pension provider is a bit of a slacker, maybe it’s time for a change. There are loads of online tools and financial advisors who can help you navigate this minefield. They’re like sherpas for your retirement mountain.

And speaking of contributions, even a small increase can make a huge difference over time. Imagine adding an extra fiver a week. That’s less than a fancy artisanal sandwich. Over 30 years, with a bit of investment growth, that fiver a week can turn into a surprisingly substantial sum. It’s like planting a tiny financial seed that grows into a money tree. A small, but sturdy, money tree.

Another surprising fact: the state pension is still a significant chunk of many people's retirement income. So, while it’s tempting to dismiss it, make sure you understand what you’re entitled to. It’s like a government-funded freebie, and who doesn't love a freebie? Just make sure you qualify!

The average UK pension pot is a fascinating, and at times, slightly alarming, snapshot of our financial future. It’s a reminder that the "future you" is relying on the "present you" to make some sensible, albeit sometimes unexciting, decisions. So, next time you’re at the café, instead of just complaining about the price of a croissant, have a quick think about that pension. Because a well-funded retirement is way tastier than any pastry. And it might even buy you more than one weekend in Margate. Who knows, maybe even a second croissant.